Archive for April 22nd, 2011

PERA – Why 8% Isn’t 8%

Posted by Joshua Sharf in Budget, Colorado Politics, PERA, PPC on April 22nd, 2011

State Treasurer Walker Stapleton has been on the hustings, touting the need for PERA reform. His oped in the Denver Post a little while ago pointed out that the fund’s actuaries assume an 8% return on investments. If we don’t do something about the underfunding, Stapleton noted, we’ll be forced to take on more risk to try to reach the fund’s investment goals.

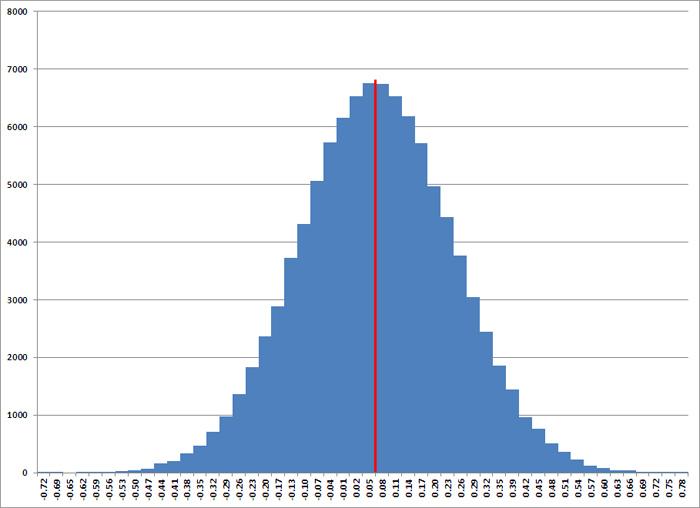

Now, PERA’s been criticized for assuming an 8% return, but that’s not really the problem. Eight percent is, in fact, the average annual return on US stocks since about 1870, according to data collected by Robert Shiller, he of the half-eponymous Case-Shiller Housing Index. The problem is, the standard deviation – the range within which about 5/8 of the returns actually fall – is 18%:

Which means that a lot of the time – almost one-third – you’re getting negative returns. For Backbone Business, I worked up a little scenario where you’re starting with $100,000, paying out certain portion each year, getting 8% return a year on your balance, and you come out even. But what should be apparent is that there are lots of scenarios that get you 8% average return, but force you to pay out more than you’re getting in the early years, and you never make up the difference. Here are some very basic scenarios:

And the graphs of the balances:

Atlas Shrugged and the Railroads

Posted by Joshua Sharf in Business, Economics, PPC, Transportation on April 22nd, 2011

Interestingly, one of the complaints that conservatives have about Atlas Shrugged is that the movie centers around a railroad. (McClatchy, too, but then, they’ll believe – or not – pretty much anything.) For some reason, they have a hard time believing that people will, or do, actually use railroads.

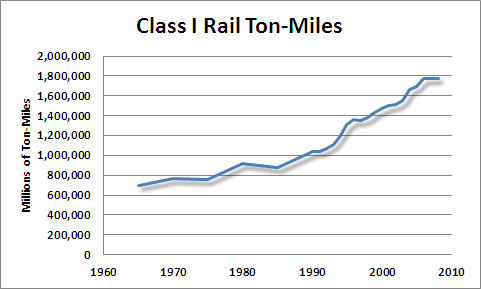

In fact, rail is increasingly important for freight, and has been on the upswing for a couple of decades now. Take a look at these following charts derived from Bureau of Transportation Statistics data. Overall Class I (major trunk line) ton-mileage stalled in the 70s, but started upward again with deregulation and the welcome death of the Interstate Commerce Commission:

?

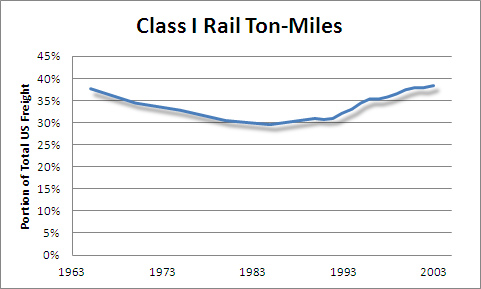

And as a percentage of total US freight ton-miles, it’s been headed up since the mid-80s:

About a year and a half ago, the Federal Railroad Administration published a report indicating that over long distances, rail is between 2-5.5x more efficient than trucking (Hat Tip: Future Pundit). I work at a trucking company, and I can tell you that intermodal – combined truck-train for long-haul shipments – is growing by leaps and bounds. Given the massive investment necessary to lay new track and secure new rolling stock, trucks continue to be a better choice for short-haul. But the best coast-to-coast operational choice seems to be rounding up the freight onto a container by truck, getting it to the railhead, and letting the train do the long-haul work. Trucks can then do the local or regional delivery at the other end. I even heard on long-time trucker complaining about this trend in the company cafeteria a few weeks ago.

I can’t remember where I saw it, but someone also poke fun at the idea of transporting oil by train. Hadn’t these people ever heard of pipelines? Aside from the apparent permitting nightmare in getting new pipelines approved, I can also tell you that the idea isn’t necessarily as ridiculous as it sounds. When were were looking at a couple of different ethanol plays at the brokerage, the need for specialized railcars was one of the drivers we took into consideration.

I initially also had thought that maybe it would have been better to focus on some newer technology rather than trains, but having seen the film, I’ve no doubt they made the right choice. Trains are visible, tangible, and connect with something very American.

The interesting thing about O’Rourke’s suggestion – that maybe they would have been better off setting the film in the 1950s – is that instead of liberating the filmmakers, it would have firmly trapped the film in past, reducing its relevance even more. Because almost everything Rand projected about trains actually happened. Unable to compete with subsidized roads, regulated to death by the ICC, trains deferred more and more maintenance, until northeast corridor rail freight virtually collapsed in the late 60s, leading to an actual government takeover and the creation of Conrail and Amtrak.

Once railroads were able to set their own rates again, they consolidated and recovered. Conrail’s operations have since been privatized, and the graphs above show the results. Union Pacific has been profitable right through the recession.

Railroads, as mentioned, do have a problem with the large capital investment necessary to expand, making them less flexible compared to trucks, just as light rail or commuter rail is less flexible compared to buses. But the idea that the country neither needs nor uses railroads just isn’t true, and fuel costs – as indicated in the film – will just make them more relevant for long-haul trips.

-

You are currently browsing the archives for Friday, April 22nd, 2011