Access Denied

Posted by Joshua Sharf in PERA on August 5th, 2013

Ed News Colorado reports on last Thursday’s State Appeals Court ruling denying State Treasurer Walker Stapleton access to dereferenced PERA data for high-salaried members:

Stapleton, a Republican, is a vociferous critic of the current PERA structure. The state treasurer is automatically a member of the 16-member PERA board. First elected in 2010, Stapleton in 2011 asked the board for access to individual records (without names) of the top 20 percent of PERA retirees, based on pension amounts.

High-dollar pensions have been something of a fixation for GOP critics of PERA, even though the average monthly benefit paid by the system is $3,020. Most PERA members aren’t eligible for Social Security. The PERA system covers all Colorado teachers and many higher education employees.

That last paragraph requires some rebuttal. High-dollar pensions are a fixation in large part because the rest of the PERA board decided to go to the mattresses to keep the information from being released. One might just as easily ask why keeping high-dollar pensions secret is something of an obsession for PERA.

That said, there are some excellent reasons for wanting to examine PERA’s high-dollar pensions.

First, at least some of those pensions come from teachers’ union reps, who are frequently no longer doing work for their school district, and instead are working exclusively for the union. The status of the Douglas County Federation of Teachers (DCFT) union rep became a major point of contention during open negotiations, mostly because she would have continued to accrue PERA benefits, even though the union offered to pay both her salary and her personal PERA contribution. With a $1 billion tax increase likely to be on the ballot this fall, and with much of the opposition to that tax increase based on the fact that about half of it would go to fund teachers pensions rather than classrooms, non-teaching union reps receiving outsized pension benefits would be embarrassing both for PERA and for tax increase supporters.

The other reason for concern over high-dollar pensions is the agency problem surrounding the PERA board itself. Most of the board are PERA members, and many receive high salaries, and so will be eligible for high-dollar pensions when they retire. With the PERA board having opposed recent attempts at reorganization, so that fewer board members are voting on their own benefits, the last thing they want is for attention to be focused on those benefits.

From a political point of view, it also makes sense for Treasurer Stapleton to try to split PERA beneficiaries between the average member and the high dollar recipient. While the PERA board and its allies have a history of resisting attempts to limit benefits overall, or to change the benefit calculation formula, a graphic demonstration of the actual distribution of benefits could lead many average PERA recipients to rebel against leadership, and accept limits at the high end of the scale. From the board’s point of view, that would be an ominous development.

While the Appeals Court has decided that Colorado taxpayers are not entitled to this information about their senior government employees, there is yet hope that the State Supreme Court will decide differently.

UPDATE: An earlier version of this post mistakenly attributed the ruling to the State Supreme Court.

Real Returns and Solvency – Part I

Posted by Joshua Sharf in PERA on August 4th, 2013

One of the biggest problems with the way that pension plans report their solvency numbers is the assumption of constant returns over the life of the plan. By assuming constant returns, plans end up hiding the single biggest factor in why they’re likely to go bust: risk. This post will try, with a hugely (and unrealistically) simplified example, to illustrate the problem this poses when trying to figure out whether a plan has enough money to cover its liabilities.

For this first cut, the aspect I want to capture is that with mandatory annual outflows, a pension fund puts itself at risk of falling behind, and never being able to catch up.

Let’s take this example: a $1,000,000 liability, timed to last 30 years, with $250,000 annual payouts, and payments into the fund that are calculated based on the expected return on assets. Here’s what the fund balance will look like if we assume a constant 8% return on assets:

Payments into the fund each year are calculated to be a little over $161,000 a year in order to make this happen. Also note that all this is being conducted in real dollars; we’re ignoring inflation, which is going to drive some people up the wall, but 1) we can always make a calculation in real dollars, 2) there’s really no good way of predicting inflation over a 30-year span, and 3) this is a thought exercise.

Where can I get an 8% a year return for 30 years? Well, I could put it in bonds that return 8%, but those may not always exist. Right now, we have a low-interest rate environment, and even corporate bonds that are highly-rated don’t necessarily return 8%. Surely investment-grade municipal bonds don’t get me 8% at 30 years. And remember, I need to find a place to put each year’s inflow, so by the end of the 30 years, I’m unlikely to find a 1-year corporate or municipal bond that pays me 8%, absent a pretty severe inflationary environment.

One investment that is liquid, that also provides reliable 30-year returns over 8%, is the S&P 500 index of large-cap US stocks. The S&P has been around since 1926. So starting in 1955, we have 30-year return profiles for it. Here’s the distribution of annualized 30-year returns for the S&P 500, from 1955 – 2011:

The thing has never returned less than 8.5% over that time, and averages 11.76% (although the median is lower). This is a period of time that covers a World War, a Depression, inflation, the Korean and Vietnam Wars, the 2000 Tech Bubble Burst, and the 2008 Real Estate Bubble Burst. That’s a pretty good track record.

Here’s the rub. Here are the annual S&P 500 returns over that time:

Not so good. You have a pretty good chance of losing money; in 11 years out of 85 you’d be down 10% or more, and in 6 of those years, down 20% or more. In three of those years, you’d lose 35% or more of your total investment. You can see the problem: the risk of running one really bad year, or a couple of moderately bad years, early on, where you might have to spend your seed corn, is high enough to be worrisome, even if the total 30-year return is comfortably higher than your planning.

In order to see our imaginary fund’s chances of making to 30 years solvent, we need to put in not a constant 8% return, but a random variable that looks like the S&P 500 annual return. Surprisingly, there’s considerable debate over whether or not such a variable is even possible to construct. The returns are clearly not normally distributed, and adding more moments (skewness, how fat the tails are, etc.), doesn’t produce unique random variables. When you look at the returns, it also looks as though the year-to-year returns may not really be independent, either; that is, a losing year seems to follow another losing year.

Given all this debate, I just figured that, with 57 separate 30-year runs available to us, the easiest thing to do would be to use those 30-year runs themselves. I.e, 1956 – 1985, 1957 – 1986, etc. Here’s a pretty typical return profile:

One really bad year, a couple of downers soon after, but positive almost all the time, and a number of eye-popping returns of over 40% to make up for it. Should work out, ok, right?

Not so much:

The actual balance in the account falls below the projection in Year 9, and never really is able to gain altitude again. By Year 20, the fund is bust, and has to either get bailed out or stop making payments.

What’s interesting is that it’s not the Year 6 Catastrophe that does the fund in. Given the good years that preceded it, the balance after Year 6 is right at the projected levels. A fund manager could easily persuade himself that everything’s going to be ok. What really causes the problem is the two bad-but-not-disastrous Years 9 and 10 consecutively. The S&P comes back in consecutive years with 20%, 25%, 20%, 35%, and it’s still not enough to put any real air between the balance and the ground. So by Year 15, when the S&P loses less than 10% – less than it had lost in any of the previous losing sessions – it’s effectively all over.

How often does this happen? Well, here are the failure rates for various return assumptions, starting with the average of 11.76% that the S&P actually returns, and going to 7%, for the ultra-conservative fund manager:

The manager who doesn’t leaving himself any breathing room cashes out over 60% of the time, which might be a little surprising. It’s not until we assume a 10% return (corresponding to annual pay-ins of $143,000), that we get to a 50-50- chance of seeing 30 years. Our 8% manager still fails over a quarter of the time, and it’s not until we get past a 7% assumed return (pay-ins of $169,000) – where we’re effectively giving up 40% of the actual S&P historical return in our planning, that we almost get to an 80% chance of solvency in Year 30.

Now, to be clear, you don’t end up in such bad shape most of the time that you don’t go bust. You’re often well in the black. For the fund manager who’s planning on 7%, he ends up over $10,000,000 in the black over a third of the time. So often, when you win, you win really big.

But in pensions as in baseball, you can’t spend those winnings from other timelines. The Cardinals beat the Reds 15-2 today, but tomorrow, it’s 0-0 when the pitcher takes the mound. My concern as a pensioner is being able to plan on a certain amount of money coming my way after I retire. If the plan goes bust when I’m 75, it’s too late for me to make other plans. And if the plan ends up with an extra $9,000,000 on-hand when I’m 80, there’s not much benefit in that, either. The cost of losing is very, very high; the unlikely rewards from extra winnings don’t make up for that, which is why I put my money into a “safe” pension plan in the first place.

Understand, as stated at the outset, this is a hugely simplified example, on about 100 different levels. Real pension plans don’t consist of a single individual. They generally don’t make payouts at the same time they’re collecting contributions. The lifetime of the plan for an individual is longer than 30 years. Their portfolio is more diversified than putting everything in US stocks. Inflation actually matters to pensions, possibly for benefits, certainly for wage calculations.

But the basic point – that the actuarial assumptions of flat returns, assumptions that fail to take into account risk as well as reward – are serious planning flaws that can ultimately lead to a plan’s demise.

My hope is, over time, to make these models more complex, remove some of the simplifications, give something approaching actual likelihoods of Colorado’s PERA going bust, and ultimately, create an online model where you, the reader, can enter your own assumptions and see what happens to PERA’s long-term prospects. That’s a big project, and it’s going to take a long time to complete. But there’s nothing in the finish product that isn’t here in the basic principles: returns move around all over the place, and the cost of providing ownership in a liability rather than an asset can be ruinous.

The PERA Fire Sale, The Gift That Keeps On Taking

Posted by Joshua Sharf in PERA on August 1st, 2013

Over at the Denver Post, Vince Carroll details the price that PERA has been paying for its “fire-sale” of pension benefits from 2001-2005:

There are many PERA beneficiaries like Coffman who bought years of service — often at a very advantageous discount — and who now receive pension checks larger than you would expect based upon the span of their careers.

A large number of those transactions occurred over a three-year period a decade ago, when “PERA conducted what one executive called, in retrospect, a ‘fire sale’ on the service credit,” according to a 2005 analysis by the Rocky Mountain News.

The administration of Gov. Bill Owens, in a major blunder, lobbied for the fire sale as a shortsighted way to encourage early retirement and infuse new blood into the bureaucracy.

As Carroll notes, this problem was known as early as 2005, when David Milstead of the late, lamented Rocky wrote about it:

But the deal got sweeter. Gov. Bill Owens, then in the early part of his first term, wanted to streamline government and bring new employees into the state work force. In 2000, with his encouragement – some say pressure – PERA cut the already-low price of purchasing extra years by 14 percent, to 15.5 percent of salary.

Owens said he doesn’t recall the specifics of what was said to PERA, but “I thought it was valuable to have the flexibility to get new employees into some of the positions in the state bureaucracy.”

…

Service-credit purchases kicked up by 38 percent in 2001, topping $100 million.

PERA decided to raise the price back to 18.1 percent of salary for members under 50 and increase it to 22.1 percent for older members. But they told employees it wouldn’t happen until November 2003.

Given that window, thousands of employees raced to the sale.

It also calls to mind an excellent article by Josh Barro in National Affairs, “Dodging the Pension Disaster,” where he suggests a way (perhaps) to actually reduce the unfunded liability after a defined benefit-to-defined contribution transition:

A working paper by Maria Fitzpatrick, a fellow at the Stanford Institute for Economic Policy Research, attempts to determine just how highly some public employees value their pension benefits. She examined Illinois teachers’ choices when, in 1998, they were offered a chance to make a one-time payment up front in exchange for more generous benefits in retirement. The terms of the purchase varied significantly depending on a teacher’s salary and years of service. Using reasonable discount rates, the up-front purchase cost was lower than the present value of benefits for nearly all teachers — 99% could expect at least a 7% annual return on investment, with no risk so long as the state did not default. But the deal was sweeter for some teachers than for others, a variation that made it possible to estimate the subjective present value that teachers placed on future benefits.

Fitzpatrick’s finding is, in a way, depressing: On average, teachers were willing to pay only 17 cents on the dollar to obtain a pension-benefit increase. This suggests that defined-benefit pensions are a highly inefficient form of compensation, costing taxpayers far more than they are worth to public employees.

But it also suggests an appealing policy solution: Governments can offer to buy back promised pension benefits at a discount, and employees may be inclined to take the deal. Admittedly, the proposal presents a political problem to lawmakers, in that it requires them to produce an immense sum of cash up front in order to eliminate a long-term liability. To alleviate some of that pain, however, governments could responsibly issue bonds to raise the money — since this would mean simply substituting explicit debt for a larger amount of implicit pension debt. Governments would incur an obligation to pay interest on the bonds, but in most cases that amount would be more than offset by the reduction in required employer pension contributions.

In Colorado’s case, the price was about 15.5 cents on the dollar, but there was huge interest, so a fair price may be considerably higher than that. Add to that the fact that people are often less willing to let go of a perceived cash benefit than they are to buy it in the first place, and there’s reason to think we can’t possibly buy it back for 15.5%. Still, having a limited-time “open season” market, or Dutch auction, with a declining price, might be a way of disposing of some of the liability.

PERA’s the price for purchasing service credit has since returned to reasonable levels, we’ll be living with the cost of selling long-term debts cheaply for a long time to come. At this point, it’s almost impossible to tell how much of PERA’s long-term debt obligation comes from this sale; I can’t find aggregate numbers in the CAFR, and the charts above show only the price paid, not the goods sold, but it certainly warrants further investigation.

President Whistled For Travelling, Moving His Pivot Foot

Posted by Joshua Sharf in National Politics on July 26th, 2013

If President Obama really is pivoting back to the economy, his political organization doesn’t seem to have gotten the message.

On Monday, at a speech for Organizing for Action, the President reinforced a White House statement that he’d begin a speaking tour, with the goal of refocusing national attention on the economy. At the time, I noticed that even as he and the White House were promoting the tour, Obama was derogating the effectiveness of his speeches:

Then, today, I got an email from OFA, asking me to set aside a day in August for one of their “Actions.” Here’s the calendar:

It’s the president’s usual list of political priorities: immigration “reform,” gun control, global warmism, and a sudden defensiveness about Obamacare, which appears to be about as settled as the “climate science.”

Not much about the economy there, is there?

Jefferson on the Declaration of Independence

Posted by Joshua Sharf in History on July 4th, 2013

May 8, 1825

But with respect to our rights, and the acts of the British government contravening those rights, there was but one opinion on this side of the water. All American whigs thought alike on these subjects.

When forced, therefore, to resort to arms for redress, an appeal to the tribunal of the world was deemed proper for our justification. This was the object of the Declaration of Independence. Not to find out new principles, or new arguments, never before thought of, not merely to say things which had never been said before; but to place before mankind the common sense of the subject, in terms so plain and firm as to command their assent, and to justify ourselves in the independent stand we are compelled to take. Neither aiming at originality of principle or sentiment,nor yet copied from any particular and previous writing, it was intended to be an expression of the American mind, and to give to that expression the proper tone and spirit called for by the occasion.

All its authority rests then on the harmonizing sentiments of the day, whether expressed in conversation, in letters, printed essays, or in the elementary books of public right, as Aristotle, Cicero, Locke, Sidney, &c. …

Indeed, the national Declaration of Independence followed dozens of state, county, local, and group declarations throughout the country, terminating the legal authority of the British regime in their own jurisdictions. It fell to Jefferson and the Committee to provide a philosophical basis suitable to a national declaration.

The form these declarations took was traditional: a letter to the King explaining grievances, declaring rights, and establishing new rules to preserve those rights. Thus they were acts of rebellion and disunion in forms that emphasized and embodied the continuity of Anglo-American political tradition.

Anyone who hasn’t read Pauline Maier’s American Scripture should do so between now and next July 4.

PERA’s Premature Celebration

Posted by Joshua Sharf in PERA on June 28th, 2013

This morning, the Denver Post carried a story about PERA’s “celebration” over a 12.9% return on its investments in 2012, and how it allegedly puts to the lie to State Treasurer Walker Stapleton’s concerns over the solvency of the pension plan.

Would that it were so, but PERA is, as usual, spiking the football on this one too early.

First, let’s start with the return itself. 12.9% is good, but it’s not exceptional, as PERA returns go. It’s above the 8% that they assume over the next 60(!) years, in order to get the funds to be solvent over that time, to be sure. And it’s only possible because a higher return means a higher volatility. As we’ve said before, PERA only needs to have a couple of bad years to fall so much further behind that it can’t catch up. This year’s modest gains in its funded levels could easily be wiped out by even a couple of average years that see positive returns in the 5% range.

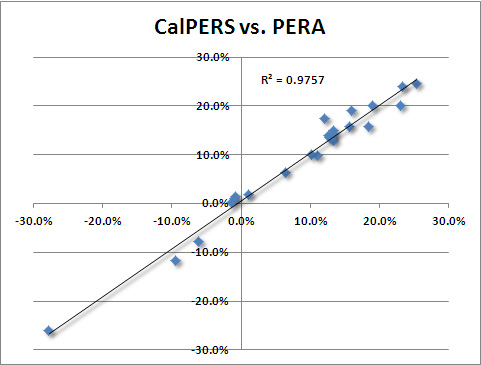

As an aside, we should also note that PERA’s returns follow the returns of the much larger California pension system, CalPERS, almost exactly:

The 12.9% is below PERA’s self-imposed benchmark of 13.4% – with Alternative Investments doing the worst relative to its benchmark. It’s right at BNY Mellon’s Median Public Fund average return of 13.0%. And it’s right in line with what you’d expect, given CalPERS’s 13.3% this past year. If PERA is willing to declare victory for missing its own benchmarks, and doing just about as well as everyone else, we should perhsaps be asking what we’re actually getting for all that money management staff we’re paying.

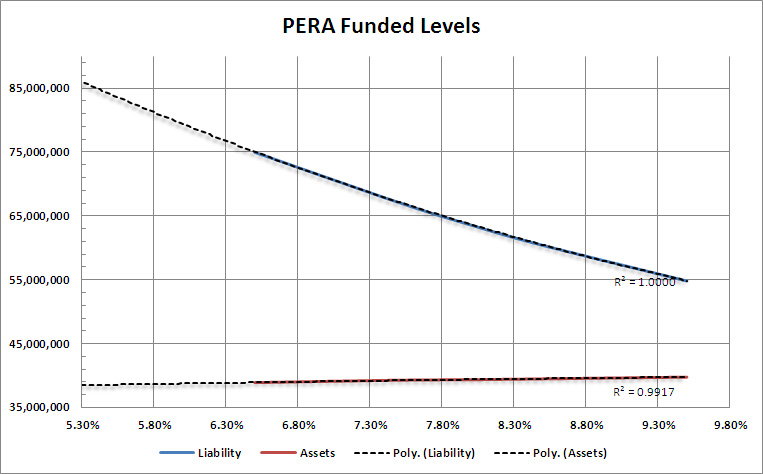

Worst, though, is that PERA’s situation really hasn’t improved all that much, and remains far worse than they’re willing to admit. PERA discounts its liabilities using the expected rate of return on its investments, per the Government Accounting Standards Board (GASB) rules. There are a number of problems with doing this, first and foremost being that it encourages funds to take on more risk in order to appear better-funded. It’s also unsound financial economics. Every other pension rule in the world requires the fund to use its parent entity’s long-term cost of borrowing. In this case, that would be best approximated by Colorado Certificates of Participation, currently trading at 5.3% yield. PERA provides a sensitivity analysis of various discount rates, and it’s not too hard to extend it back to a rate of 5.3%. (There’s also a very slight change in the actuarial value of the assets; I’ve included that just for completeness).

So basically, properly calculated, instead of having the unfunded liability of just over $24 billion that PERA admits to, it’s actually in the hole for about $47 billion, or about $23,500 per household. A more accurate number could be gotten with a more detailed analysis, but this is probably within a billion or two dollars, which suddenly doesn’t seem like all that much money.

PERA likes to claim that the actual unfunded liability doesn’t really matter all that much, since it can’t ever be called in tomorrow, but must wait until it’s actually due. Like so much else PERA says when it comes to its unfunded liability, this fundamentally misunderstands the nature of present value. The point isn’t whether or not a liability can be collected tomorrow. Present Value is just a means of comparing a future liability and present assets in today’s dollars, a way of asking how much you would pay today for the promise of the amount of the liability tomorrow (or whenever it’s due). It has nothing to do with whether or not such an immediate transaction is possible.

However, we can calculate how much the unfunded liability will mean to Colorado families when they have to make it up. Right now, a $23,500 debt, paid at PERA’s assumed return of 8% over 30 years, is about $2,000 per family, per year.

Save the champagne.

As relates to another story – PERA’s baleful effects on school budgets, the release of the CAFR gives us a chance to update our school spending charts. There’s some improvement in the growth rates, even as they continue to far outpace inflation. And in the School Division, the increase is coming entirely from the taxpayers.

The US Supreme Court’s Proposition 8 Ruling, and TABOR

Posted by Joshua Sharf in Budget on June 26th, 2013

Today, in its ruling on California’s Proposition 8, the Supreme Court ruled that citizens’ groups do not have standing to defend a law passed by referendum or initiative in federal court, should the state decline to do so. By making this reasoning the basis for its decision, the Court has potentially invited grave implications for Colorado and its Taxpayers Bill of Rights.

Currently, TABOR is the subject of a lawsuit arguing that it violates the US Constitution’s provisions that each state have a republican form of government:

The United States shall guarantee to every State in this Union a Republican Form of Government, and shall protect each of them against Invasion; and on Application of the Legislature, or of the Executive (when the Legislature cannot be convened), against domestic Violence.

ARTICLE IV, SECTION 4

The plaintiffs, which include five current Democratic state legislators, argue that, by removing the legislature’s ability to raise taxes without approval by the people, has violated that clause. That case is now in federal court, in front of the 10th Circuit Court of Appeals.

That assertion has been challenged on a number of counts. First, the federal courts have ruled that clause – the “Guarantee Clause” to be non-justiciable, leaving it instead as an issue for the political branches. Second, there is every reason to believe that the founders used the word “republican” to describe even systems of direct democracy.

Currently, with Gov. Hickenlooper named as respondent on behalf of the state, Colorado’s Attorney General, John Suthers, is defending TABOR on behalf of the state.

In the case today regarding Proposition 8, Hollingsworth v. Perry, the State had declined to defend Proposition 8 in court, despite its having been an approved referendum, and being the law of the State of California. The Supreme Court ruled that, in the absence of state defense, private citizens groups cannot do so in its stead. Once the state agrees with the plaintiffs, the court was essentially saying, there is no case.

The implications for Colorado’s TABOR case, and next year’s elections to succeed Suthers as Attorney General, are profound. While any or all of the Republican candidates can be expected to defend TABOR vigorously, the election of a Democrat would open the possibility that the Colorado Department of Law might decline to defend TABOR in federal court.

In the case involving the Defense of Marriage Act, the federal Department of Justice declined to defend DOMA in court, but the US House of Representative hired counsel to do so. If the Democrats were to retain control of both houses of the state legislature, it is highly unlikely that they would act to defend TABOR in this way.

If that were to happen, TABOR might be left without defense, and without any party with standing to conduct a defense. In short, a twenty-year-old state Constitutional Amendment, whose basic provisions have never been overridden on subsequent attempts at repeal or modification, could be killed by default.

Clearances

Posted by Joshua Sharf in Uncategorized on June 12th, 2013

For those who are wondering what a 29-year-old with a GED was doing with clearances, I actually know something about this. I had TS/SCI, with various compartments within a specific type of program, before I was 25. None of that was unusual.

I also had a bachelor’s in physics & math, but that was needed for my job. Evidently, for Snowden’s computer work, he had skills in demand. He had whatever tickets they felt he needed to do the computer work he was hired to do. So while this was obviously a failure from a vetting point of view, there’s nothing about his age or his skills that a priori points to a problem.

Senator Wyden (who evidently tried to trap DCI Clapper into revealing the existence of the NSA program in open session) has also made much of the contractor/employee division, implying that contractors are somehow at greater risk for this sort of thing to happen.

This is also overblown. I was always a contractor, once for a company whose primary client was in Langley. There was cultural friction between the “blue badges” (employees) and the “green badges” (contractors), to be sure. There was a difference in pay, and there was also a difference in the type of work they did. The employees did the actual analysis, for the most part, while the contractors did the programming and the support work.

There was never any sense that contractors were inherently less trustworthy or loyal to the country. We had passed the same polygraph tests, after all. But we were clearly outsiders, who hadn’t made the sacrifice of joining the Company, and so were always more temporary.

There is no reason to believe, and nobody at the time believed, that contractors were more likely to be careless with security, or to go trotting off to our primary adversaries, portfolios tucked under our arms.

The NSA Phone Warrants, Reconsidered

Posted by Joshua Sharf in War on Islamism on June 7th, 2013

How bad is the revelation that the NSA is collecting phone call information on pretty much every call in the country?

I’ve had a lot of fun on Facebook making fun of the NSA Phone Records Extraction, Acquisition and all-Knowing (Phreaking) program. In the current context, that sort of dark humor is entirely appropriate for the somewhat casual, breezy atmosphere of social media. A more serious appraisal is required here.

So, here are some of the better discussions I’ve seen in the last few days:

- Powerline: Is the NSA’s Collection of Phone Records a Scandal?

- Lawfare: What Conceivable Statement of Facts Could Have Produced this Order?

- Lawfare: DNI Statement on the Verizon Story

- Volokh: Is Verizon Turning Over Records of Every Domestic Call to the NSA?

- Jonah Goldberg: Time to Dial Up Some Healthy Skepticism

- WSJ: Thank You for Data-Mining

- Taranto: Snoopy, Come Home!

- Foreign Policy: Why the NSA Needs Your Phone Calls

They represent a variety of opinion, and Lawfare in particular is going to have its teeth into this for a while. Keep going back to it and Volokh for serious legal and policy reporting.

I mentioned above that in the current context, dark humor is called for. This administration has demonstrated a truly unique talent for politicizing just about every aspect of a formerly professional civil service. Therein lies the danger of the current context.

As a conservative, and not a liberal or a libertarian, I want the War on Terror, or War on Political Islam, if you prefer, to be pursued as a war, not as criminal investigation. It’s the main reason I want Gitmo to stay open, since we can interrogate enemies there without certain restrictions that they’d have here on US soil. We need to figure out how to make sure that the government has the tools it needs to prosecute that war without being able to turn them on us.

This is tricky work, with plenty of judgment calls, trial and error, and changes of rules as some thing work and others work too well. It’s the hard work of making government work, and having the discussion start with, rather than end with first principles.

Angela Giron, IRS Beneficiary

Posted by Joshua Sharf in Colorado Politics on June 4th, 2013

Well, what do we have here?

Colroado State Senator Angela Giron (D-Pueblo), facing a recall from voters in her district over her gun control votes in this year’s state legislature, has gotten considerably monetary help from outside sources in her bid to stay in office, the Pueblo Chieftain reports:

Giron, a Pueblo Democrat, is the target of a recall drive by Pueblo-area gun rights supporters and Republicans. Her defense campaign, called Puebloans for Angela, received a $35,000 contribution from the Sixteen Thirty Fund in Washington; a $20,000 contribution from a Denver organization called Citizens for Integrity; and a $15,000 contribution from a Denver group called Mainstream Colorado. (emphasis added – ed.)

The Sixteen Thirty Fund has been organized as a 501(c)4 since Feb. 16 of 2009 (we wonder how long it had to wait for IRS approval), according to its 2009 IRS Form 990, and its mission, as state on Page 2 of that documents is:

Sixteen Thirty Fund operates exclusively for the purpose of promoting social welfare, including, but not limited to, providing public education on and conducting advocacy regarding progressive policies.

The fund operated as a collector and distributor of over $3.3 million for various left-wing causes during 2009, including $52,000 to our very own Progress Now here in Colorado. It won’t come as any surprise that most of those groups, including ones that are clearly political organizations, are also organized as 501(c)4s.

Now, I don’t have any problem with these or any other groups organizing as 501(c)4s, if the law allows that. But it’s telling that Democrats have decided to turn the various IRS hearings into a trial of the tax law, one which they were perfectly happy to take full advantage of as long as the other side didn’t. Having kept Tea Party, conservative, and libertarian groups on the sidelines through two election cycles, they can now afford to be outraged at unfair treatment, and call for a revision of the law.

And of course, there’s this, from Senate President John Morse, fighting his own recall battle:

I intend to fight this – we cannot allow outside interest groups to determine what is best for Colorado. #coleg #copolitics #GunSafety

— John Morse (@SenJohnMorse) June 4, 2013

-

You are currently browsing the archives.