Archive for March 13th, 2013

Forty Years of PERA

Posted by Joshua Sharf in Budget, Colorado Politics, PERA, PPC on March 13th, 2013

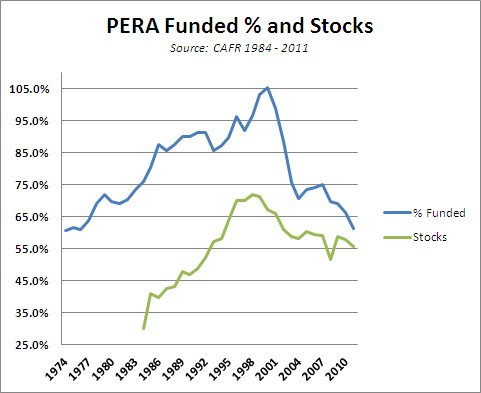

We’ve been here before with PERA. Sort of. Most people following the issue remember that in 2000, PERA was over 100% funded, and that its funding ratio has fallen steadily since then. What they don’t know is that back in 1974, PERA was woefully under-funded, at about the same 60% funded ratio that it is now. It took advantage of the long bull market to pull itself out of that situation:

Note that as the funded ratio rose, so too did the percentage of the portfolio allocated to common stock (both domestic and foreign) rose, as PERA basically decided to let the bets ride, rather than re-allocate to maintain the lower-risk portfolio. When the bubble burst, they ended up paying the price for having stayed too long at the fair. Now, PERA has returned to a somewhat more conservative allocation strategy, targeting 25% of its money for fixed income, and a target of 58% in stocks. Nevertheless, this is a far cry from the 45% or so in bonds that they held up until 1992 or so, and the nebulous “Alternative Investments,” which includes things like venture capital (and in which I’ve included the Lumber investments), suggests that PERA is still chasing yield there:

So this just puts us back where we were before, right? We climbed out of this hole before, we can do it again.

Not so fast. First, as noted before, PERA’s in a less aggressive portfolio now than it was in 2000. This is a good thing, since it takes out some of the volatility from its portfolio. But it also means that it probably can’t count on a run of good luck to lift it out of unfundedness the way it did last time. Also, as we’ve previously noted, the fall from grace in 2001 and 2002 wasn’t just a matter of poor returns, it was also a matter of increasing liabilities with more generous benefits. That hasn’t gone away.

And not all 60% funded ratios are created equal. Here are PERA’s inflation-adjusted, per-capita unfunded liabilities since 1974 (constant 1983 dollars):

On a per-capita basis, the overhang is about 4x what it was in 1974. So in fact, we’re in much, much worse shape than we were 40 years ago when this roller-coaster ride began.

-

You are currently browsing the archives for Wednesday, March 13th, 2013