Welcome, Instapundit readers! While you’re here, take a look at posts on Certificates of Participation. Perhaps your state has something similar…

On Thursday, November 8, the Jefferson County School Board voted to ask teachers participating in its Supplemental Retirement Program to take a buyout for what would amount to about 64 cents on the dollar.

By following other public pension systems into what amounts to a default – albeit partial – JeffCo Public Schools join the parade of cautionary tales for those relying on the promises of public programs like PERA. As Glenn Reynolds of Instapundit is fond of reminding us, promises that cannot be kept, won’t.

History of the Plan

Quoting from a 2009 RFP for a plan financial advisor (emphasis added):

The Supplemental Retirement Plan was created in 1999 for employees who worked in full-time or job-share positions which were covered by an association. It was designed to replace a bonus-type program for retirees who met age and service requirements, with a tax-advantaged vehicle. Benefits are intended to supplement, not replace, PERA retirement benefits. Participation in the plan was immediately frozen upon its creation.

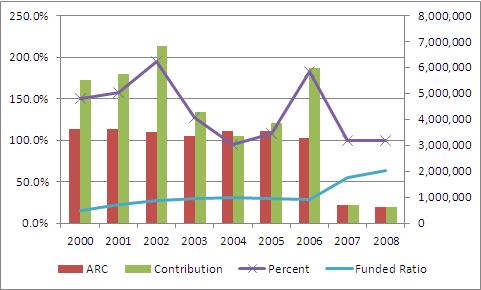

The District had originally committed to fund $90 million dollars toward a combination of pension plan benefits and sick and personal leave payouts at a rate of $9,000,000 per year for 10 years. However, budget cuts reduced the annual plan contributions and stretched out the plan’s original funding timetable. The plan has been underfunded since its creation. In 2007, the District purchased certificates of participation and deposited the funds into the plan for the purpose of meeting its stated funding obligations and has now exceeded its original funding commitment. Further contributions to the plan are not likely to be made. Subsequently, existing retirees and employees who met the full vesting requirements of 20 years of eligible service and age 55 were offered a one-time ability to have their benefits satisfied with a lump-sum payout at the plan’s stated discount rate. As a result, participant count, liabilities and assets have decreased in the plan and the overall funded status of the plan has improved. It is anticipated that at some point the plan will need to declare actuarial necessity and terminate or reduce plan benefits for non-vested participants. After the lump-sum payouts, the plan amended its investment policy to be more conservative, in an effort to protect the funding of benefits for existing retirees and vested participants.

The plan wasn’t underfunded for lack of district contributions. According to the latest available plan financials, also from 2009, the district met or exceeded its annual contribution every year until 2009, with the exception of a slight shortfall in 2004. The combination of payouts and lower-than-necessary returns kept the plan funding under 32%, until the 2006 issuance of $37 million of Certificates of Participation (more about that in a coming post) reduced the outstanding obligations starting in 2007.

As of the 2009 report, the plan had $20.8 million in obligations, $7.4 million of which were unfunded.

Issues with Transparency

There appear to be a number of significant transparency issues with the way the plan has been handled.

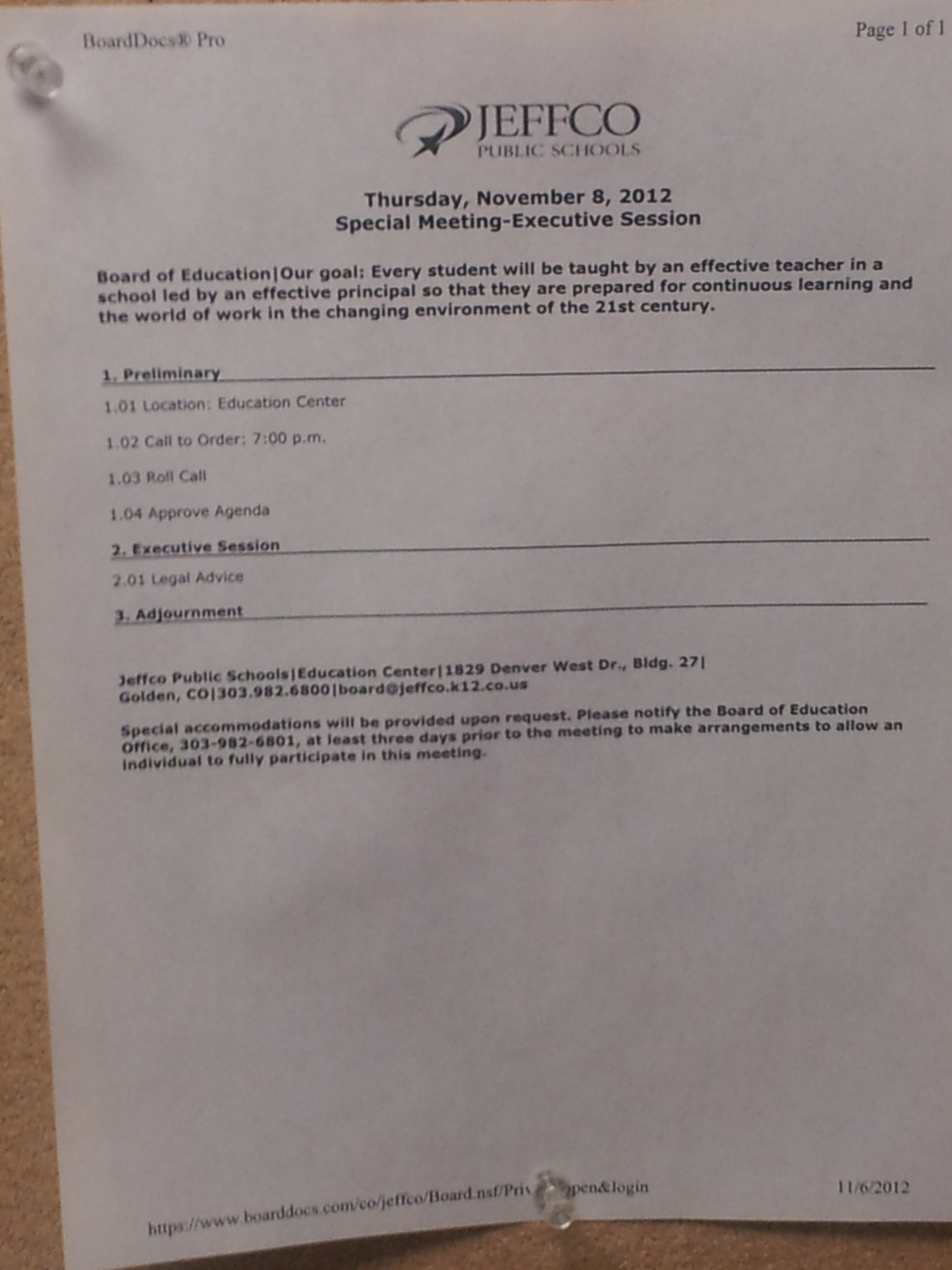

The November 8 meeting itself raises issues of transparency and obligations of full disclosure to the public. The meeting discussion was held in a 45-minute executive session. Executive session is supposed to be reserved for legal advice, not for general discussion of motions before the Board. It is unthinkable that the Board received a 45-minute legal briefing, after which it proceeded directly to a vote.

Moreover, at least the topic of an executive session is required by law to be posted in advance of the meeting. Here’s the notice that was posted outside the Board’s meeting room the evening of November 8:

There is, evidently, case law to suggest that the recording of the Executive Session should therefore be made public, since the session – although not the vote – were conducted in violation of statute.

The most recent financials available online date from 2009, three years ago. Even in the absence of significant financial changes, plan financials from the most recent year should always be available.

Also note that the teachers were offered a buyout in 2006 – which the smart money, including current Superintendent Cindy Stevenson took – the 2009 statement RFP for a plan financial advisor all but admits that the plan will terminate and default on the remaining obligations at some point. Whether or not this likelihood was made clear to the teachers who chose to remain with the plan in 2006 is unclear. What it clear is that Stevenson, and possibly current Board member Jill Fellman, were made whole during the 2006 buyout offer, while other teachers were not.

UPDATE: According to the FY2011 Comprehensive Annual Financial Report, in 2011, the Board decided to terminate benefits for anyone who hadn’t reached the thresholds of age 50, and 20 years of service as of the end of the 2011 plan year, 8/31/2011. “The plan is still operational for active and deferred vested participants and beneficiaries in receipt of payment.” It is those members who will be asked to take a cut in their benefits. The district has also “determined that additional contributions for the foreseeable future would not be made to the Plan.” (Note 16, P. 72)

The funded ratio has fallen to 50.6%, and the unfunded liability as of August 31, 2010 is $8.8 million.

Correction: No vote was actually taken at the November meeting. (I left early because of the descent into executive session.) It is likely that there will be a vote at the December or January meeting. Stay Tuned.