Archive for category Business

WalMart Hatred and Racism?

Posted by Joshua Sharf in Business, Economics, PPC on July 9th, 2012

I don’t tend to post a lot on purely social issues. But there are times when the two issues intersect in their own very illuminating way. During the June 26 hearing on the Colorado Health Care District redevelopment, one gentleman, one of three African-Americans in the room, took exception to some of the concerns being expressed by the neighbors of the proposed project:

“I’m a civil rights activist and a member of this community. I have family and friends who live here in this community. I’m here tonight – I thought I came here for peace and unity. But I see, that’s not going to be the case. Why? Because I sit over there, stood over there, and heard you all use all these buzzwords and code words. ‘We don’t want that element out here. We don’t want our property values to go down. Those are code words to say we don’t want black and brown people…”

(Shouting and yelling)

“You say ‘No,’ then why don’t you…”

“We don’t want the people who shot the police officer.”

“You know something, I don’t either, I don’t want them either, and I’ve stood on the front line saying put his butt in jail. But at the end of the day, what I’m saying is this. You want to be fair about it, Wal-Mart has been a friend of the African-American community, and I think that it will continue to be a friend to our community, and we need their help, and we need your help.”

Right after he finished, one of the audience members yelled after him something about Wal-Mart keeping wages down. But that wasn’t his point. His point was twofold: first, without Wal-Mart, many of those people wouldn’t have jobs at all, and second, Wal-Mart keep prices down, making many things more affordable to people with lower incomes.

Now, I don’t think most of the people in the audience were consciously racist. But I do believe that the charge stung precisely because, as good liberals (the precincts surrounding the development voted from 75% to 85% for Obama in 2008), they believe themselves to be incapable of racism. And to be sure, their bias isn’t the kind that leads someone to put on the bedding and burn crosses.

But it is paternalistic. They are unable to imagine that they have neighbors who can’t afford the options they’d put in the place of WalMart, and who would welcome a WalMart in walking distance. And they were stunned to hear from a black man that he very much wanted something that they were convinced he had no business wanting.

Almost 60 years ago, Billy Wilder had Humphrey Bogart, in the character of Titan of Industry Linus Larabee, explain things to his ne’er-do-well kid brother, William Holden, in the 1954 Paramount picture, Sabrina:

Wilder wasn’t a corporate shill. In The Apartment, he showed that he understood as well as anyone how to satirize the business world. But this is a lesson that many of those yelling about Wal-Mart that warm evening might bear in mind.

A Bridge Loan Over Troubled Waters?

Posted by Joshua Sharf in Business, PPC on June 22nd, 2012

As mentioned yesterday, the Denver Democrats have invited Rep. Maxine Waters to speak at the annual State House District 7 Unity Dinner this Saturday night. While we think Waters is a terrible excuse for a Congressman, she’s all-too-representative of her party in at least one respect – a belief that it’s possible to give money to one person without taking it away from someone else.

As the interview deteriorates from a policy discussion into Waters’s patented grievance-mongering, CNBC’s redoubtable Mark Haines former analyst and Erin Burnett go from incredulity to resignation, that they’re dealing with someone with roughly a 1st grade understanding of accounting. In fact, you can only arrive at her beliefs through a rigorous process of re-education; 1st grade math problems routinely feature apples being taken away from Johnny and given to Timmy.

In the past, HD7 has invited Mayor Michael Hancock, Auditor Dennis Gallagher, and Speaker Andrew Romanoff. Say what you will about them, they have the virtue of being adults. Hancock and Gallagher have demonstrated fiscal common sense in their positions with the city, and while we’ve had our disagreements with Romanoff in the past, he at least demonstrated some understanding of economic and fiscal matters. (Who knows? Maybe she’s even one of the idiots who needs educating?)

People like Hancock, Gallagher, and Romanoff have actually had responsibilities to larger groups that have pulled them to the center, in rhetoric, if not always in deed. Waters, with a safe seat in south-central, has the luxury of indulging her worst impulses on a regular basis, and probably isn’t the ideal figure for a broad-based party to unify around.

If the Denver Democrats insist on inviting folks like Maxine Waters to keynote these dinners, perhaps they need to rename them the Fragmentation Dinner.

Investments and the Two Minutes’ Hate

Posted by Joshua Sharf in Business on May 30th, 2012

I’m smart enough to realize that there’s no power on earth, aside from maybe Frank Capra, that can make a bank an object of sympathy. But yesterday’s Two-Minutes’ Hate outside Wells Fargo’s main Denver office sure came close:

When the call went out, this was the focus on ProgressNow’s email:

Over the last four years, Wells Fargo’s federal income tax rate was just 3.8%–less than what nurses, firefighters, teachers and janitors pay–despite making some $69.1 billion in profit. If Wells Fargo had paid their fair share in federal taxes, Colorado would have received an extra $53 million–money to hire hundreds of teachers, nurses and firefighters.

The source for this claim seems to be a Citizens for Tax Justice report, claiming to show that Wells Fargo actually got back $680 million, on $49.4 billion in profit, from 2008-2010, and then applying the same methodology to 2011.

There are many flaws in the CTJ’s study, beginning with the idea that while the tax expense isn’t real, somehow its “current” component is more real than its “deferred” component. It’s a mistake that they have a history of making, especially in years following recessions and election years, when the difference between financial accounting and tax accounting depresses apparent tax rates. It’s a mistake that Megan McArdle and Fortune have caught the New York Times making as well.

Cash, on the other hand, is real. Cash represents an actual check that Wells Fargo wrote to the Federal government. So while the IRS wasn’t writing Wells Fargo a $4 billion check in 2009, the company’s Statements of Cash Flows do say that on $64 billion of net income, it wrote checks to the government for $11.7 billion over those four years. To the extent that this represents “real” taxes paid, it constitutes an 18% tax rate.

But here’s one of the most revealing claims:

“…’accelerated depreciation’ is technically a tax deferral, but so long as a company continues to invest, the tax deferral tends to be indefinite.”

And the problem with that is…? Evidently “investment” only counts if it’s government “investment” in Solyndra, or if it’s the result of shakedowns by community “organizers,” like the ones on the streets yesterday, or the one the White House. Wells Fargo claims a quarter-billion dollars a year in charitable and community giving, but of course, that’s them deciding what to do with their money, and if it doesn’t satisfy the avarice of SEIU organizers, or fall under their control, then it doesn’t count.

Remember: Progressively More Expensive, Progressively More Intrusive, Progressively More Restrictive.

An Evening With Arthur Brooks

Posted by Joshua Sharf in Business, Economics, PPC on May 23rd, 2012

Also last night, Susie and I went to go hear Arthur Brooks of the American Enterprise Institute speak, at the Young Americans Center for Financial Education. The Center is truly a wonder, set up to teach grade schoolers about business, finance, and economics. Brooks spoke in Young Ameritowne, a large hall set up like a town square, ringed by mock storefronts – sponsored by actual businesses – that the kids role-play at operating. Go see it. (Now if they could only devise a program targeted at state legislators, we’d be golden.)

The failure of conservatism and free-market forces to arrest the country’s leftward drift for almost a century now should be of profound concern, and should be a puzzle to those of us fighting the fight. AEI was founded in 1938. Go back and read some of the Intercollegiate Studies Institute’s journals from the 1950s, 60s, 70s, and you’ll see two types of articles. One it the neo-confederate and near-neo-confederate type, of which we are well rid, and which come from a world as alien as Gilbert & Sullivan.

The others are those that could have been written any time in the last four years, changing only the names of the programs and actors. Those arguments didn’t carry the day back then, yet we expect that they’ll work this time.

Why, when all the empirical evidence is that socialism doesn’t work, capitalism does, that less freedom produces greater misery, why have we been losing the fight for 100 years, since Wilson’s election? This despite poll after poll that shows that Americans continue to embrace capitalism under that name, and reject redistributionism, by overwhelming margins?

This question has been bothering me for well over a year now, because even with all the intellectual ammunition at our disposal, it doesn’t bode well for this fall, or for what comes afterwards, with so much at stake. And too few conservatives and libertarians seem to be asking it at all.

What a relief, then, that someone with Brooks’s intellect has recognized the same problem, and what a pleasure that he’s actually got a persuasive answer.

Brooks is such a clear thinker and gifted speaker that I can reproduce the bulk of his argument from memory a day later, and I have a terrible memory. He gives you just what you need to remember, and he gives you the pegs to hang it on. When Susie and I saw him speak at the Western Conservative Summit in 2010, we thought his was far and away the best talk of the weekend.

Brooks contends that both the liberal answer – that Americans secretly want socialism – and the conservative answer – that all we need is better data – are flawed, because they don’t address the moral arguments that people find persuasive.

What we’ve been missing is a moral defense of capitalism, one that doesn’t take an 1137-page hardback “novel” to summarize. Moral arguments deal with people, and arguments that deal with people are always more persuasive than arguments that deal in numbers. Too often we dismiss that sort of thinking as “feelings over facts,” but Brooks contends, correctly, I think, that that’s a mistake. It’s how people actually come to conclusions and make decisions, and winning the argument means reaching people on their terms, not making it necessary for them to come to us.

Brooks’s case consists of three parts:

1) Earned Success. That is what truly defines happiness, not mere wealth. Earned success means linking success and its rewards to talent and effort. When results are decoupled from action, you get, “learned helplessness,” a recipe for unhappiness and frustration, since you’ve learned that you can’t really control your future.

2) Fairness. Conservatives like Milton Friedman resist talking about fairness, largely because we think it’s too subjective. But it’s also persuasive, and those same polls that show people love capitalism also show that they crave fairness. Well, what could be more fair than letting people keep what they earn, and decide how to use their own wealth? It’s a critical battlefield, one we can own, but not if we don’t show up for the fight.

3) Capitalism is good for the poor. Mere wealth may not be the measure of happiness, but poverty is a pretty good measure of misery. And it’s capitalism that reduces the misery that is a hand-to-mouth existence, not socialism, not all the good intentions in the world.

Moral defenses of capitalism abound. From Michael Novak’s The Spirit of Democratic Capitalism, to Hayek’s The Road to Serfdom, people have been thinking for generations about why a free system is a better system. But Novak is an academic, and neither Americans nor Europens feel tyrannized by the welfare state. The Greeks may yet provide a contemporary illustration, but thus far, most people see serfdom coming from the barrel of a gun, not a food stamp debit card.

The beauty of Brooks’s defense is that it not only speaks about people, it speaks to people, on terms that relate to their lives. It does it without policy prescriptions that strike people as weird, or re-opening arguments that were dealt with 170 years ago, when we decided we didn’t like polygamy and did like internal improvements.

The YA Center promptly violated 1) and promoted learned helplessness by giving out copies of Brooks’s new book, The Road to Freedom, which promises to tighten up the argument, and explain, for instance, why direct help with the best of intentions can have very bad results.

I’m looking forward to reading it, and reviewing it.

How Would You Sell The Tea Party?

Posted by Joshua Sharf in Business, Movies, National Politics, PPC on March 22nd, 2012

Reading Malcolm Gladwell’s What the Dog Saw, I got to his essay, “True Colors: Hair Dye and the Hidden History of Postwar America.” He argues that the difference between Clairol’s “Does She or Doesn’t She?” and L’Oreal’s “Because I’m Worth It,” is the difference between 1950s and 1970s feminism. Moreover, even when the two product’s pitches had essentially merged (Gladwell was writing in 1999), their buyer’s different self-images lingered on. Smart ad men know they’re selling more than a product, they’re selling an experience, or an image. Sometimes, that image or dream ties into a larger social change or movement, and that that’s both a reflection and an agent of that change:

This notion of household products as psychological furniture is, when you think about it, a radical idea. When we give an account of how we got to where we are, we’re inclined to credit the philosophical over the physical, and the products of art over the products of commerce…

“Because I’m worth it,” and “Does she or doesn’t she?” were powerful, then, precisely because they were commercials, for commercials come with products attached, and products offer something that songs and poems and political movements and radical ideologies do not, which is an immediate and affordable means of transformation.

Far from trivializing a political, social, or economic movement, commercialization can help make it personal and accessible, and therefore less threatening and more familiar.

We’ve seen a couple of Tea Party movies, one explicitly so, (Atlas Shrugged), and one implicitly (Robin Hood). Thus far, I’m aware of only one commercial that implies a Tea Party presence, the Starbucks commercial with the angry old loner who yells at town halls, which would be a bit like L’Oreal selling “Because I’m worth it” using Nurse Ratchet or Gloria Steinem, who quickly became a caricature of herself.

It may be that we have to wait until the Tea Party sees more success, in winning hearts and minds if not yet national elections, before companies are willing to bet their products’ success on its messaging. But just as feminism succeeded in making the political personal (and more destructively, the personal political), and as environmentalism succeeded in making small actions and then products green, the Tea Party might get farther by doing something similar for its own themes.

It’s not wise to choose your political message based on the products it might sell, but certain themes will sell better than others. We can search forever in the tall grass of social history to discover how much of feminism’s public appeal was based on opportunity, and how much drew from raging against The Patriarchy, but there’s no question that positive sells. Ilon Specht may have been angry when she wrote, “Because I’m worth it,” but the slogan expresses liberation, not anger.

To be sure, it faces some hurdles in doing this. If the theme is fiscal responsibility, most families already need to spend less than they make. If it’s personal liberty, the government’s probably a tougher customer to disobeying rules, tougher than most companies. And to the extent that it dwells on what used to be, rather than what might be, its message is nostalgia, and the only products it will sell are baseball and Coca-Cola. You want to get people to invite your ideas into their homes, you need to be relevant to how they’re living their lives today, and want to be living them tomorrow.

So, what products do you see as being right for capturing the Tea Party ethos, and allowing people to internalize it? Which themes are best suited to commercialization? And what messages should go in their commercials? How would you write such a commercial?

Chronicles of Crony Capitalism

Posted by Joshua Sharf in Business, Finance, PPC, President 2012, Regulation on February 23rd, 2012

So far, the LightSquared story has mostly been written as one of the FCC favoring a politically-connected company at the expense of its competition, and that favoritism having resulted in nothing but waste. See, for example, today’s Coffee and Markets podcast on the subject. Their related links (Documents: LightSquared shaping up as the FCC’s Solyndra and Documents show Obama’s FCC used regulatory muscle to destroy LightSquared’s competition) pretty much give the outline. It’s a simple story, and one that fits in neatly with an overarching narrative, as they like to say, of political money buying regulatory help.

As usual, the story is more complicated than that. And as usual, the full story makes things look even worse.

The Wall Street Journal ran a story discussing just how badly the FCC had tied itself up in knots over this. First, they declared a looming bandwidth shortage, and then quickly auctioned off additional spectrum, spectrum that happened to lie near to that used for GPS. This was done years ago, and Falcone and his people no doubt assumed that the FCC wouldn’t be selling spectrum that couldn’t be developed. Having gotten the favor, they then were surprised when the FCC didn’t turn around and tell the GPS people that this was coming, and that they should shield their equipment – technically well within their capability. Having failed to do that, they now have to argue that there’s no spectrum shortage, after all.

Even assuming that the FCC wasn’t out to clear the field for LightSquared, they failed badly in their regulatory duty here. The FCC has complete control over this stuff. They can decide how, where, and when spectrum gets exploited, and by whom. Either there is or isn’t, was or wasn’t, a spectrum shortage that will imperil future growth. Either the spectrum neighboring the GPS wavelengths is or isn’t usable. Either the burden of preventing interference lies with LightSquared (or whoever buys this tainted real estate from them), or it lies with the GPS companies.

Either the FCC didn’t know how it was planning to resolve this issues, or didn’t care. Or else, it knuckled under to a multi-million dollar lobbying campaign, in which case, what’s the point of claiming “independent” regulatory agencies are any good at all? If the FCC was throwing around its weight to help LightSquared, all these regulatory conflicts become even worse, leading other investors to throw their money after an investment the FCC must have known was headed for an iceberg.

The other example comes from the Department of Transportation:

Transportation Secretary Ray LaHood announced a $54.6 million loan to Kansas City Southern Railway Company (KCSR) for the purchase of 30 new General Electric ES44AC locomotives. These diesel-electric locomotives, built in Erie, Pennsylvania, will help KCSR meet increasing economic demand, and are more energy-efficient and produce significantly less carbon emissions than the locomotives they are replacing.

That’s nice. Railroads have had a very nice couple of years, and with the absence of KeystoneXL, are likely to have even more business, at least in the short term. Kansas Southern has a $7.8 billion market cap. It’s already carrying $1.6 billion in debt. Its quarterly depreciation expense is almost $50 million, or just about the size of the loan. Its operating cash flow was $170 million last quarter, and it showed a net income of $300 million. And it’s not as though GE is going to file for bankruptcy protection if it doesn’t get a $50 million order.

This from the same administration who reflexively defends a perfectly reasonable accounting change (see The Death of LIFO) by attacking oil companies, rather than by defending the change on its own merits.

The problem with both of these stories is that the finance is bound up inextricably with the politics. Analysts work by examining the underlying economic return, and to the extent that there are regulatory issues, they ought at least to be predictable or bounded. Companies getting regulatory benefits they can’t use, or subsidies they don’t need, don’t do anything to help create real wealth.

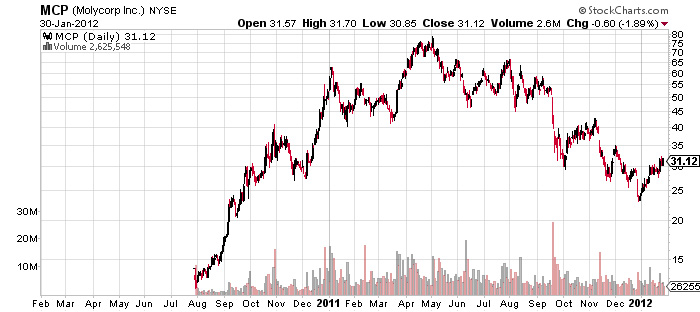

How Not To Manage Rare Earths

Posted by Joshua Sharf in Business, Economics, PPC on January 30th, 2012

Rare earths were in the news a lot in 2011. Right now, it seems as though the news coverage paralleled the bubble in prices, but there’s no reason to be complacent. The government continues to make mistakes in dealing with these resources, missing opportunities to do it right, and eventually costing not only the taxpayer in cash, but also the country in national security.

First, a refresher on what rare earths are used in:

Late in 2010, Colorado-based Molycorp announced that it was ready to reopen one of the world’s richest rare earth mines in California, about an hour south of Las Vegas. The stock price soared, and soared even more on the news that it was working on vertical integration with a prime use of rare earths, magnets for wind turbines. Then, in mid-2011, China announced that it would begin cutting back on its rare earth quotas. Initially interpreted as China throwing it weight around, it now is clear that they were simply responding to demand information that they, as a near-monopoly, had before everyone else.

The metal prices themselves have followed suit, in a number of cases down well over 50% from their mid-2011 highs:

Some of this was simply a bubble bursting, but it’s also possible that the catalyst was more than just an amplified cyclical downturn. Vestas, along with a number of other wind companies, has found out that government subsidies aren’t forever, as the Spanish, Germans, and even the Americans are cutting direct subsidies to wind turbines. At the same time, other mines are increasing output, with Chile’s molybdenum output up 11% in 2011, and Toyota is threatening to release a rare-earths-free Prius. Rare earths prices are starting to stabilize, and it’s hard to see them going much lower.

While the world figures out a way around the problem, the US continues to throw environmental roadblocks in Molycorp’s way to actually re-opening the mine. Cong. Coffman’s well-intentioned proposal is to create a strategic reserve. By the time the bill actually passes, prices will quite possibly have risen again, and it’s not as though, in the long run, companies lack the incentive to retrieve these metals from the ground. To the extent that this is a national security issue, the solution is to let the companies mine the damn things, and to develop an ongoing industry capable of supplying the country’s needs, not only to guess as what we might need and stockpile them.

Sun Sets On Solar

Posted by Joshua Sharf in Business, Energy, PPC on November 15th, 2011

Chinese solar manufacturers, heavily subsidized by the Chinese government though they are, are not completely immune from the laws of economics. Faced with falling demand, falling prices, and growing inventories, they’re cutting production. The follows on the heels of a number of high-profile failures of solar manufacturers here in the states.

True that the Chinese government, in its relentless mercantilism, was, and is, subsidizing solar heavily enough that three of their companies may survive the shakeout, whereas it’s possible none of ours will. But in fact, they were just responding to a market that largely existed because of European and American solar subsidies in the first place. The collapse of solar prices isn’t about new manufacturing techniques (yet), it’s about Europeans realizing that not only is the energy more than they can afford, so are the jobs, and they’re mostly going overseas, anyway.

The irony is that we’re still being told that we need to “invest” in solar because the Chinese are committed to it, and that must validate the idea. It turns out that the Chinese were only invested in it because they figured to have us as their high-priced customers. Not only were we funding both sides in the solar arms race, we were using the result to justify nonsense subsidies like Solyndra and LightSquared. It’s like one of those experiments where the monkey reacts to itself in the mirror. Only in this case, it was more like Lucy and Harpo pretending to fool each other.

Colorado, under former Governer Bill Ritter, began to pursue a “New Energy Economy,” chasing and subsidizing alternative energy companies, hoping to lure them to the state. Ritter was elected in 2006, and the financial meltdown and succeeding recession created revenue shortfalls that limited the damage he could do. The latest brouhaha over missing funds at the Governor’s Energy Office hasn’t done their cause any good, either.

The ideologues won’t be swayed, of course, but perhaps many of the more pragmatic politicians can be persuaded that these are bad bets for governments to be making.

President Golf Calls You Lazy – Again

Posted by Joshua Sharf in Business, Economics, PPC, Regulation on November 14th, 2011

In what was called a “scripted conversation” with Boeing’s CEO James McNerney, Jr., President Obama reprised his Malaise Moment of a few weeks ago, and said, “We’ve been a little bit lazy, I think, over the last couple of decades,” which resulted in the 2009 dropoff in Foreign Direct Investment in the United States.

I have to admit that my first reaction was that I was too busy to be bothered with replying. But, as the saying goes, sharks gotta swim and bats gotta fly.

Taken at face value, I don’t have any idea what the hell he was talking about. Worse, I don’t think he does, either. Certainly even a cursory examination of the facts would reinforce the conclusion that Obama’s grasp of recent economic history isn’t any better than his grasp of mid-century diplomatic history.

Below is a quarterly graph of foreign direct investment in the United States, starting in 1980. The series starts in 1960, but it roughly zero from then until 1980, owing to the fact that the US, generating the lion’s share of the world’s wealth, was relying on exports more than FDI for growth:

You can see a couple of patterns here. First, FDI accelerates through the business cycle, as expected. As the economy picks up steam, it generates interest abroad and confidence in investors looking for growth. Second, over the last “couple of decades,” FDI has grown through each business cycle, if you discount the dot-com bubble evident in the very late 90s. Third, when the US economy goes into recession, foreigners stop investing here, until they see some evidence of a bounce-back. All of these patterns clearly apply to the most recent recession, and the current economy.

Of course, we all knew this was bunk, anyway. National accounts must balance, and the only way we can finance our trade deficit is through FDI in our economy. If we find ourselves unable to generate enough wealth, or attract enough investment, to import the things we want, that’s indeed an indictment of our ability to compete, but it likely has much more to do with government policy and regulation than with the work ethic of most Americans.

Obama’s statement that this pattern existed over “the last couple of decades,” is, I think, an attempt to include Bill Clinton’s presidency in his criticism, a back-handed return volley to Clinton’s oblique criticisms of Obama’s economic policies. It’s more than just his routine scolding of his fellow citizens, it also contains a domestic partisan political component, as well. One wants to resist the temptation to overstate the electoral consequences of such tension. But it may be that the President’s famously thin skin is once again getting the better of his judgment.

At this rate, maybe his staff should just use that XtraNorml animation engine for any future “scripted conversations.”

First Thing, Let’s Crash All The Banks

Posted by Joshua Sharf in Business, Finance, PPC on October 31st, 2011

The latest idea from MoveOn.org and their friends and OWS is to withdraw all their money from the “Wall Street Banks,” and to move it to smaller, community banks and credit unions on November 5th. If such a move were to take place on the scale they’d like, it would be a deliberately created bank run on the largest financial institutions in the country. They seem to have gotten the scheme from some Ron Paul supporters, who are at a minimum mildly ticked off that OWS and MoveOn are claiming credit for it.

They may claim that this is a small, symbolic action, but that doesn’t excuse it. Small, symbolic actions are unlikely to have any actual effect on large institutions, and fanatics don’t propose such actions hoping for them to be merely symbolic.

We can all be grateful that this won’t amount to a hill of beans in this crazy world, but this is still a terrible idea, one whose ineffectualness doesn’t absolve it of its fundamental irresponsibility. You might expect this sort of thing from MoveOn, but the Ron Paul people fancy that they understand how banks work, and that turning all of Wall Street into the Fidelity Fiduciary Bank wouldn’t be the soundest financial strategy. Bringing Wells Fargo crashing down isn’t any better an idea now than it was 3 years ago, and it’s liable to take a bunch of smaller, “safer” community banks with it.

The basic premise of the exercise is flawed. It’s certainly true that the balance sheets of some of the larger banks are in worse shape than many smaller, community banks. And it’s equally true that Too Big to Fail probably means Too Big (to borrow a phrase from Instapundit), and that any bank Too Big To Fail should probably be broken up into smaller entities. And when smaller banks fail, they fail less catastrophically.

Ironically, the website for the Move Your Money Project features a scene from “It’s a Wonderful Life,” the bank run scene, on a building and loan that, if you remember, came within $2 and the goodwill of a couple of neighbors of failing.

Smaller banks do fail, almost 300 between 2009 and 2010, and 86 so far this year. The MYMP site will cheerfully direct you to a smaller bank or credit union, one which stands a good chance of operating under some sort of enforcement action from the Office of Thrift Supervision, the Office of the Controller of the Currency, the Fed, or the FDIC.

Ultimately, this isn’t about “sending a message” to Wall Street, or making your money safer. It’s about visceral hatred of banks and bankers, and a failure to appreciate the role that finance plays in a healthy capitalist system.

Yaron Brook, who runs the Ayn Rand institute and is nobody’s idea of a Keynesian squish, has the appropriate response:

-

You are currently browsing the archives for the Business category.