Archive for category PPC

A Challenge to My Democrat Jewish Friends

Posted by Joshua Sharf in National Politics, PPC on June 19th, 2011

Swing by the Baltimore Center for Jewish Education on Saturday, but don’t bring your children. Wear a yarmulke or bring something that distinguishes you as Jewish. Stay for a while. Listen to the speeches. Normally, I’d also advise walking right up to the front door and trying to enter the building, but it’s Shabbat, so the CJE is closed

If you’re not in Baltimore, there should be other, similar opportunities all over the country, although most of those won’t be targeted at Jews in particular so much as Whitey in general. Yes, the New Black Panthers are at it again.

Afterwards, let your friends and neighbors know about the warm, non-intimidating reception you got.

And then ask yourself – again – why Eric Holder didn’t think that white voters in Philadelphia were intimidated, and decided to drop a case he had already won:

Greeks Bearing Grifts

Posted by Joshua Sharf in Business, Economics, Finance, PPC, Regulation on June 16th, 2011

And if the threat of starvation and a southern land rush weren’t enough here on Disaster Wednesday, there’s always Greece:

…But conditions in European markets are deteriorating. The main risk from Greece has always been contagion, and that process is already under way.

Most directly, prices of Portuguese and Irish bonds have fallen sharply, with 10-year yields rising above 11% and the cost of insuring their debt at record levels. The gap between Spanish and German 10-year bond yields is at its widest since January. The market is effectively giving no credit for any reforms or budget policies set out in the past six months.

The next link in the chain, the banking system, has been affected. In Spain, progress by banks on regaining market access has gone into reverse: Average borrowing from the European Central Bank jumped to €53 billion ($76.32 billion) in May from €42 billion in April.

Meanwhile, the contagion into core banks may be being underestimated by investors. Moody’s on Tuesday said it could downgrade France’s BNP Paribas, Société Générale and Crédit Agricole due to their holdings of Greek debt, and the ratings firm is looking at whether other banks could face similar risks.

Disturbingly, the worries have now reached non-financial companies, which have been virtually bulletproof this year. Investment-grade bond issuance has come to a near-standstill.

I seem to remember having seen this movie before, as the prequel to to 2008’s Episode IV: A New Hope. It may provide some cold comfort to Americans that this time, it’s taking place in Austrian, even if Germany’s pending LBO of the rest of Europe isn’t the Teutonic Shift the President had in mind a couple of weeks ago.

But there’s no particular reason to be complacent. Just as we’ve managed to convert our economy from fast-falling to encased-in-amber stasis, we could be in for another financial shock. Megan McArdle suggests one route: (I hate to quote a post in almost its entirety, but it’s short, and I don’t think I can say it better)

During the wave of banking regulation that followed the Great Depression, the government slapped heavy controls on the interest rates that banks could offer. They weren’t very good, which made the banks sounder, and consumers worse off. When inflation and interest rates rose in the late sixties, this became a big problem. Then some clever chap came up with the money market fund. Legally it worked like an investment fund, not a bank account: you invested in shares, with each share priced at a dollar. The fund invested in the commercial paper market and committed to keep each share worth exactly one dollar; whatever investment return they got was paid out as interest on your shares. This gave you something that looked a lot like a bank account, without all the legal tsuris.

In 2008, it turns out that these money market accounts were–as was always pretty obvious–a lot more like bank accounts than mutual fund shares. The Reserve Primary fund held a lot of Lehmann Brothers commercial paper, which plunged close to zero, meaning that there were no longer enough assets in the fund to make all the shares worth at least a dollar. This is known as “breaking the buck”, and it was not the first time it had happened. But it was the first time in more than a decade that it had happened at a fund which didn’t have enough money to top up the assets in the fund to bring them back to a value of $1. Bigger investment houses had been quietly topping up their money market funds for month, but Reserve Primary was a smaller firm, and they didn’t have the spare cash handy.This triggered a run on the money markets, which the government really only stopped by a) passing TARP and b) guaranteeing money market funds. But as Matt Yglesias points out, Dodd-Frank stripped Treasury of the authority to do such a thing again. And now the money markets are exposed to a Greek default.

Something like 45% of US Money Market funds have some direct exposure to Greek debt. Greece defaults, and many of these funds may be breaking the buck without Big Ben backstopping for them.

But that’s only the direct exposure. Then, there’s the indirect exposure, though insurance, and (probably) Credit Default Swaps:

Finally, it’s worth noting that once you account for the substantial payouts that US agents will have to make to European creditors in the case of a default by one of the PIGs, financial institutions in the US have roughly as much to lose from default as those in France and Germany. (See the figures in blue in the table above.) The apparent eagerness of US banks and insurance companies to sell default insurance to European creditors means that they will now have to substantially share in the pain inflicted by a PIG default.

The risk to US banks itself may be small, but the effects of having sold this insurance, and of people finding out that they sold this insurance, could be substantial:

The big US banks are well-capitalized now, and can fairly easily absorb losses of several billions of dollars in the event of a Greek default. But two serious concerns remain. First, I fear that this may have the potential consequence of exacerbating the flight to safety that will happen in the event of Greece’s default; if you have no idea who is really going to be on the hook and ultimately liable for CDS payments, your best strategy may be to trust no one. I don’t think that triggering post-traumatic flashbacks of the fall of 2008 is going to do good things to the market or the economy. Second, I wonder if there’s a public relations disaster just lying in wait for the big US banks. After all, how will you feel (assuming you don’t work on Wall Street) when you read the headline that Big Bank X lost money because it sold billions of dollars of credit default insurance while it was on taxpayer life-support? Rightly or wrongly, I’m guessing that Big Bank X will not be very popular for a while.

This also doesn’t address the US banks’ exposure to the European banks, the ones that may go under when Greece finally decides to call it quits. They may have positive exposure to those banks, and find that holdings in them, or loans to them, are suddenly less liquid than they had hoped.

There’s one other issue that I haven’t see addressed anywhere, and that’s the question of securitized Greek debt. Remember that we thought the subprime crisis could be “contained,” because subprime mortgages were such a small portion of the overall mortgage market, never mind the credit markets as a whole. Then it turned out that the subprime assets were poisoning entire classes of securities, since they were so highly leveraged. Is it possible – and this is purely speculation, I really do not know the answer to this – it is possible that people have done the same thing with sovereign debt, and that there are CDOs out there with Greek debt incorporated into them? Securities that could suddenly default, even though they only contain a small mix of drachmas in there?

Carmen Reinhart and Ken Rogoff point out that after every financial crisis, governments find themselves with significantly higher debt, as they seek to stop the dominoes from falling. The potential exists for European governments to become dominoes themselves, and if McArdle is right, there’s some risk (probably small, but hard to say how much) that won’t even be able to step in again and keep our own house in order.

Snow Shovel-Ready

Posted by Joshua Sharf in Energy, PPC on June 15th, 2011

Michael Mann may get some use out of that hockey stick yet.

After a particularly quiet solar minimum, solar physicists are preparing for the possibility that sunspots may be scarce for a while:

Hill’s own research focuses on surface pulsations of the Sun and their relationship with sunspots, and his team has already used their methods to successfully predict the late onset of Cycle 24.

…Hill’s results match those from physicists Matt Penn and William Livingston, who have gone over 13 years of sunspot data from the McMath-Pierce Telescope at Kitt Peak in Arizona. They have seen the strength of the magnetic fields which create sunspots declining steadily.

Three different methods all confirm that we’re headed into uncharted solar waters, potentially rivaling the Maunder Minimum, which coincided with a particularly severe 70-year stretch of the so-called Little Ice Age:

Naturally, the headline writers have seized on the term “Ice Age,” with the result that people who only read the headlines think that they’re likely to wake up one morning in 2025 only to see that the massive 10-ft wall of blue ice has finally sealed them into their homes for good.

In fact, the Little Ice Age may have been a regional phenomenon, affecting the northern hemisphere. OK, yes, that’s where most of the land is, and, yes, that where most of the people live, so this isn’t necessarily good news by any stretch. Cooler periods tend to be drier and less fertile, although better for ice skating on wide, frozen rivers. But we don’t know the magnitude of the effect of diminishing the sun’s input. It certainly seems counter-intuitive at best to argue that the earth will be just as good if not better at capturing the sun’s heat when there’s less of it coming in.

Sure, the Hockey Puck has one hockey stick that can state with certitude that less heat from the sun absolutely, positively, won’t make any different whatsoever in the earth’s climate, which seems a little silly to me, inasmuch as it gets colder at night. But most actual scientists, you know, the ones who aren’t going around trying to suppress their model, data, or emails, recognize that the climate is a complex chaotic system, and that even small changes in the inputs can result in huge and sudden variations in the output.

And the changes in the inputs may not be as small as the Nittany Lyin’ wants to assert:

In a recent paper in Geophysical Research Letters, solar physicist Karel Schrijver of the Lockheed Martin Advanced Technology Center in Palo Alto, California, and his colleagues argue that during the Maunder Minimum, the sun couldn’t have dimmed enough to explain the Little Ice Age. Even during a prolonged minimum, they claim, an extensive network of very small faculae on the sun’s hot surface remains to keep the energy output above a certain threshold level.

Not so, says Peter Foukal, an independent solar physicist with Heliophysics Inc. in Nahant, Massachusetts, who contends that Schrijver and his colleagues are “assuming an answer” in a circular argument. According to Foukal, who presented his work yesterday here at the summer meeting of the American Astronomical Society, there is no reason to believe that the network of small faculae would persist during long periods of solar quiescence. In fact, he says, observations between 2007 and 2009, when the sun was spotless for an unusually long time, reveal that all forms of magnetic activity diminished, including the small-faculae network.

What’s more, detailed observations from orbiting solar telescopes have shown that the small faculae pump out more energy per unit surface area than the larger ones already known to disappear along with the sunspots. So if the small faculae start to fade, too, that would have an even stronger effect on the total energy production of the sun. “There’s tantalizing evidence that [during the Maunder Minimum] the sun may have actually dimmed more than we have thought until now,” Foukal says.

Let’s assume, just for argument, that we’re in for a century’s worth or so of cooling temps. That would imply that just about every policy we’re pursuing right now to prevent “climate change,” is both ineffectual and mistaken. Instead of eating our food, we’re burning it for fuel. Instead of expanding our energy resources, we’re constricting them, just at the time when some natural gas might come in handy on those cold, dark, May nights.

Most of these policies are easily reversible, given the will, but Global Warmism has become such an idee fixee on the part of the political class and its bought-and-paid for scientists that they’re more than capable of looking at a cooling thermometer (as it has been for the last 13 years), and declaring that nothing’s changed. Self-trained to see nothing but warming, and certain that they’ll be insulated from any ill-effects, the political class will, like their predecessors in Soviet Ag Policy, declare that every crop failure or shortage is a result of “special circumstances.”

I’m not sure I place any more faith in NASA’s complex models just because the results are sort of comforting and sort of intuitive. (There’s a reason Easy-Bake Ovens don’t work very well.) That has to go for the other side, as well, but then, that would require a level of intellectual honesty that a dependence on a government-funded viewpoint precludes.

So expect this report – and any actual observations that James Hanson sees fit to print – to change the political debate over climate change not one bit. But for those paying attention, a climate science that’s been maundering about quite a bit on its own is likely to get some very interesting data over the next few decades.

GE, We Bring Bad Ideas To Light

Posted by Joshua Sharf in 2012 Presidential Race, Business, Economics, National Politics, PPC, Stimulus on June 15th, 2011

In a prior post, I mentioned that Obama’s favorite courtier CEO, Jeffrey Immelt, was part of a Jobs & Competitiveness Council, ostensibly tasked with finding ways to put Americans to work. It’s the kind of thing that government always says it’s doing, anyway. After all, we have a Commerce Department, a Labor Department, an Education Department, and dozens, if not hundreds, of bureaus, agencies, subalterns, and fiefdoms devoted exclusively to this problem.

From the bureaucracy’s point of view, they’ve spent decades of time, billions of taxpayer dollars, and millions in campaign contributions to get where they are, and they’re not going to let a hand-picked set of toadies show them up. The beauty of it is that either their success or their failure shows that our actual redundant population lives and works within 10 miles of the Capitol.

If by now anyone at all has any faith left in this kind of commission, it should be put to rest by its initial recommendations.

I Don’t Know. The Administration Has Seemed Pretty Shovel-Ready To Me From Day 1.

Posted by Joshua Sharf in 2012 Presidential Race, Business, Economics, National Politics, PPC, Stimulus on June 14th, 2011

By now, you’ve probably seen this rueful admission by President Obama – evidently part of a longer comedy routine – that the stimulus didn’t actually do much the stimulate:

Over at Powerline, Scott Johnson takes Obama to task for laughing at unemployment, and imagines Obama & Immelt as the new Hope & Crosby, and suggests The Road to Tripoli as a working title for their first picture. I was thinking The Road to Serfdom or The Road to Ruin, myself.

In all seriousness, though, isn’t this just a president who realizes he has a real vulnerability, and is trying to laugh at it, at his own error? Is this reallly all that different from Bush pretending to search the Oval Office for the WMDs, the video for the White House Press Dinner that had the lefties in a snit a few years back?

Obama’s lousy at it, because he takes himself too seriously, and really can’t laugh at himself. I’ve never seen him do it, anyway. Bush had great comedic timing and a real sense of humility.

Of course, as an indictment of his competence, it’s far worse than Bush’s joke. Bush’s knowledge was limited to what his intelligence apparatus brought him, his perceptions were shared by the rest of the world. Many argued against going into Iraq, but virtually nobody thought Saddam wasn’t building or maintaining an arsenal of WMDs.

Obama not only got the macro wrong (Germany, for instance, has made different fiscal choices), but also, in the most generous interpretation of these comments, didn’t even bother to do due diligence about where the next couple of generations’ money was going when he spent it. A less generous interpretation – consistent with the Alinskyite acolyte – is that he knew perfectly well that it was going to bureaucrats, and now wants to be seen as fixing the problems that he himself created.

The press conference was the rollout of the first half of Obama’s so-called Jobs & Competitiveness Council, the “fast action” steps, in favored courtier co-chair Jeffrey Immelt’s words. But that’s for another post.

Fewer Workers, More Claims

Posted by Joshua Sharf in Budget, Colorado Politics, PPC on June 13th, 2011

I’ve written a couple of times about the sorry (i.e., bankrupt) state of Colorado’s Unemployment Insurance program. Well, here’s why:

??

Source: Department of Labor, Weekly UI Claims Report

This is a chart of the number of employed workers divided by the number of continuing and new UI claims, as reported weekly, through May 21 of this year. This represents, in some sense, the coverage of UI payments by the cash flowing into the fund. If you’ve read a paper anytime in the last two years, this doesn’t tell you much new about our immediate situation.

First, the caveats. Unemployment insurance claims are incredibly seasonal, and reported weekly. The number of employed used in that report appears to change only quarterly. So I’ve taken the bumps and ridges out of the data by using a 6-month backward-looking/6-month forward-looking moving average. This is not for predictive purposes, it’s just to smooth the data out for graphing, and by doing it that way, I avoid the time lag of a trailing moving average.

And, of course, the leading part of the average goes away inside of 6 months from the end. That’s important, since the seasonal downtick in claims (or uptick in ratio) may not be done yet, making it look as though the ratio is cresting again when it’s not.

A couple of interesting facts emerge, aside from the record torpor.

We forget just how great – and how anomalous – the late 90s were for Colorado. Look at the slope of that line beginning in mid-1996, and look at the plunge it takes starting in 2000. As fondly as we remember the job market here through 2006, the ratio of workers to recipients never got back to 1997 levels, never mind early 2000. Still, the UI fund was taking in more than it was paying out, even as it was levying annual solvency increases on Colorado businesses.

The seasonal variation is also much less over the last several years, indication the sense of stasis the economy has had. Layoffs are down, but so is hiring:

The right-hand axis is total employment; the left-hand unemployment claims.

As in the rest of the country, we’re at an inflection point on the graph. Also, like the rest of the country, our unemployment insurance program is likely to stay broke for a while, no matter which way things go.

We’re #7!

Posted by Joshua Sharf in Colorado Politics, PPC on June 12th, 2011

Which is sort of good news. Except that a couple of years ago, we were #2.

I’m talking about the Mercatus Center’s Freedom Index. If you think you see a pattern in that map, by the way, your eyes are not deceiving you. Blue states tend to be darker, red states tend to be lighter; the authors provide a few charts correlating liberal/progressive vote share with the different measures they use that comprise the index. Since the index lags events by two years, we still have a couple more years of all-Democrat rule to go, so things are likely to get worse for the Centennial State before they get better.

So, for the record, here’s how Colorado has fared in the 2009 and 2011 surveys:

| 2009 | 2011 | |||

| Rating | Rank | Rating | Rank | |

| Fiscal Policy | 0.21 | 5 | 0.176 | 5 |

| Regulatory Policy | 0.12 | 11 | 0.039 | 25 |

| Economic Freedom | 0.337 | 3 | 0.215 | 10 |

| Personal Freedom | 0.084 | 16 | 0.088 | 8 |

The authors have a pie chart in the back of the report showing how much weight they gave to the individual issues comprising each index.

It’s not hard to see where Colorado’s fallen down, and where it’s held up. Fiscal policy has been restrained by TABOR, and by a peculiarity that assigns greater freedom to greater revenue decentralization. In Colorado’s case, that may be a bit deceptive, as the state still mandates a fair amount of local spending. On the other hand, they do take a hard look at debt/personal income, and Colorado’s definitely headed in the wrong direction there. (The state, localities, and special districts – I’m lookin’ at you, FASTER – have all been violators here on that score.) In fact, spending as a percentage of personal income did increase over the two years covered, but the index was held in check by lower government employment as a percentage of the total workforce. When the survey comes out for 2009-2010, those trends are certain to reverse.

Personal freedom has seen both gains and offsetting losses, and you can see that the rank there improved more by comparison than by actual objective improvements. Reductions in alcohol taxes were offset by increased local restrictions on guns, but other than that, little changed from 2007 to 2009.

The authors blame the passage of a minimum wage law for much of the Regulatory Policy decline – and that really has fallen in absolute terms. Looking at the actual data, it appears that stricter worker’s compensation requirements, along with a higher percentage of workers being covered, is responsible for the rest of the decline in labor freedom. Health freedom also declined as a result of greater requirements placed on the small group market and increased mandates on policies.

The authors admit to a certain amount of subjectivity in their metrics. They use a lot of parametric tests (1 = by land, 2 = by sea, etc.), and some of the cutoffs are judgments calls. But there’s no reason to think they’re gaming their own system, looking for inconvenient cutoffs that would disadvantage some states while helping others. And there’s certainly no reason to think they’re trying to rein in Colorado’s previously stellar rankings.

Also, remember that Mercatus could fairly be characterized as an economic-based, libertarian-minded center. They tend to see public policy more as an economic measure than a social one, leading them to reflexively oppose so-called “victimless crimes,” and count, for instance, mandatory legal residency checks as an impingement on freedom, where others might see them as the price of maintaining a level of order and civility in society.

Still, it’s dismaying to see Colorado slipping in these rankings, especially when the slippage is due almost entirely to increased fiscal irresponsibility and increased regulatory burdens, practically designed to discourage job creation. If the states are the laboratories of democracy, Colorado’s recent experiments have produced some pretty decisive results.

In For The Long Haul

Posted by Joshua Sharf in Business, PPC, Transportation on June 6th, 2011

Well, this is interesting. From Burlington Northern Santa Fe’s AAR reports from the last two years:

Coal, as you can see, makes up about half of car loadings, and that’s headed down. Just from the couple of years, it looks as though there may be some seasonality in Intermodal, falling off in the last quarter. I’ll know some more when I look at Union Pacific (back to 2002 and also mostly western) and CSX (back to 2006, but mostly the northeast and south). Intermodal has improved through this year, but coal has been dropping for about 6 months.

Since the beginning of the year, coal has decoupled – so to speak – from the rest of loadings, which have climbed slightly or stayed level, even as coal has dropped. We export a great deal of coal, and BNSF serves the western half of the country, Mexico, Canada, and the Gulf of Mexico. (The railyard north of downtown Denver is a BNSF railyard, although we have a fair number of UP lines through the state, too.) There have been reports that China’s been slowing down, and nobody really trusts – or should trust – the official numbers coming out of there. Is it possible that fewer coal loadings as a sign of slackening Chinese demand?

I’m not quite sure what to make of the stagnating carloads combined with the improving outlook for intermodal. We know that, over long distances, trains are more efficient than trucks. Intermodal will continue to grow as a percentage of both rail traffic and overall freight ton-miles. Is it possible that this is just more inefficiency being wrung out of the system? Any other ideas?

Not Keeping Pace

Posted by Joshua Sharf in Colorado Politics, PPC on June 3rd, 2011

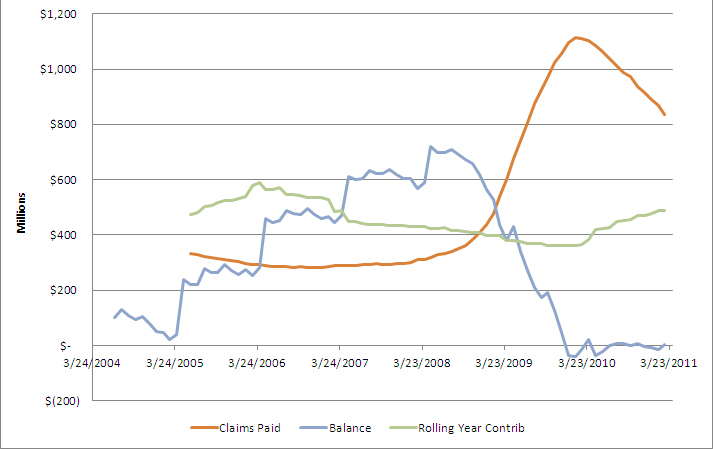

Back in October 2009, I wrote a piece examining the state of Colorado’s Unemployment Insurance Fund, and concluded that making long-term changes in eligibility in return for some short-term federal crack cocaine cash was a terrible trade. There was a graph showing where our unemployment insurance fund was headed at the time, even before federal aid, and I use that term advisedly:

The “Claims Paid” is a rolling 12-month total, as are the contributions. Well, here’s that graph now:

Colorado Unemployment Insurance Fund

As you can see, the federal “aid” didn’t arrest the decline, it didn’t even hide the decline. At the beginning of 2010, Colorado’s bank balance hit $0.00, went past that, and had stayed there ever since. That $127 million that was so valuable and necessary funded the system for about 5 1/2 weeks at the peak of claims, about 8 weeks now.

These changes weren’t just an extension of benefits. Those extensions were supposed to be picked up by the feds. No, the $127 MM was in return for structural changes designed to permanently increase eligibility. Part of the justification for the increase was Mark Zandi’s claim that unemployment insurance payments had one of the highest multipliers of all forms of intervention. But it’s been pointed out that Zandi never explained how he got to that number, and the models used have never been subjected to outside scrutiny. Moody’s is no piker, but if policymakers are going to use their results, their models need to be subject to the same scrutiny that we give to global warming data. Cough.

The business contribution line, you’ll notice, has been rising. Well, that’s not because so many more people are employed now in Colorado than used to be. It’s because every May, CDLE is allowed to levy additional assessments on business when the fund falls below a certain level. Given that levels are those for a reservoir in Death Valley, the fund right now will meet any insolvency test you care to invent.

So now, when the federal government begins charging Colorado interest for the money loaned for the further benefits extensions, and when levels remain elevated at least in part because the terms for qualifying are more generous, Colorado is back asking (in the sense that the Stasi “asked” you not to make that joke, please) for even more money from businesses.

Ironically, the House sponsor of this financial wizardry was the man who now wants you to send him to Washington for more of the same – Rep. Sal Pace. Someone from our enterprising media, someone who does this sort of thing for a living, really ought to ask him about this, dontcha think?

-

You are currently browsing the archives for the PPC category.