Archive for category Colorado Politics

Democrat Disillusionment

Posted by Joshua Sharf in 2012 Presidential Race, Business, Colorado Politics, National Politics, PPC on October 7th, 2012

Wednesday night, Mitt Romney punctured the balloon that was Barack Obama’s inflated reputation as a debater and communicator. I guess having a hollow core and thin skin is a bad combination.

Romney did this largely by turning out not to be the stick figure that Obama had been running against for the last 18 months, and which he had apparently internalized as actually being the actual Mitt Romney. So in some respects, the left’s and the Democrats’ disillusionment with Obama is a result of Obama’s disillusionment with the opponent his campaign constructed for him. So far, his only response has been to complain that Mitt the Man is a better candidate than Mitt the Myth, and to argue that Mitt must have been lying during the debate. Romney’s campaign has responded with an ad calling Obama on his own campaign’s admission that Romney’s proposed net tax cut won’t be any near $5 trillion, an admission echoed by the media “fact-checkers” that, up until now, Obama had held up as the Gold Standard of Absolute Truth.

That said, some of Obama’s own claims during the debate turn out to be at least misleading. At one point, during an answer ostensibly about working across the aisle, Obama mentioned three free trade agreements passed in 2011:

“That’s how we signed three trade deals into law that are helping us to double our exports and sell more American products around the world.”

But of course, Obama inherited those free trade agreements – with South Korea, Panama, and Colombia – from the Bush administration, and he sat on them for over two years before submitting them to the Republican-controlled House, where they were approved, and the Democrat Senate, where they passed overwhelmingly. In this regard, the comparisons with President Clinton are instructive. One of Clinton’s first acts was to submit NAFTA for Congressional approval, where it passed a Democrat House largely on the strength of Republican backing, and against the wishes of the Democratic majority. The Democrat leadership simply wasn’t going to submarine a brand-new Democrat president on one of his first initiatives. Obama had the option to do the same thing anytime during his first two years in office, but chose to wait until the demands grew loud under a Republicans House to do so.

His claims to being open to Republican ideas have always been a sham, but in this case, they’re little more than an attempt to cover up for the fact that he all but ignored economic growth and job creation for his first two years in office. The difference between Clinton’s & Obama’s trade policy lies in contrast to the similarity in their politics, though. Clinton has tried mightily to take credit for the benefits of a welfare reform bill that he only adopted once his party lost control of Congress. Likewise with Obama and these bilateral trade agreements. (In what would be a bizarre claim for an actual news organization, the Washington Post at the time tried to spin this as a win for Obama, rather than his bowing to reality.)

Closer to Colorado, Congressman Ed Perlmutter apparently never got the message, and was the one member of Colorado’s Congressional delegation to vote against all three agreements. Colorado’s trade with Panama and Colombia is relatively small, but we export hundreds of millions of dollars a year in goods to South Korea, an economy which, while running a trade surplus, isn’t nearly the export-driven economy that it used to be. Perlmutter was the only Colorado representative who professed to see a threat to local jobs in these agreements. Even Diana DeGette, long in the tank for the unions, only opposed the Colombian agreement.

As we progressively disabuse ourselves of illusions regarding Democrats, perhaps the next two to fall will be that Obama deserves credit for free trade, and that Perlmutter understands the topic at all.

June 1998 Video of Obama on Political Coalitions and the Working Poor

Posted by Joshua Sharf in 2012 Presidential Race, National Politics, PPC, President 2012 on September 24th, 2012

The Daily Caller has posted the unedited audio of then-State Senator Barack Obama at a Loyola College forum, where he discusses the importance of uniting the working poor with welfare recipients as a political coalition.

Turns out this wasn’t a one-off, or a cool idea that occurred to him in the middle of the forum, but something he had been thinking about for a while. Here’s C-SPAN video of him at a Brookings Institute forum on the State of the Cities four months earlier, on June 14, 1998:

Why is this problematic? Traditionally, the working poor haven’t identified with welfare recipients, but with the middle class, just as the middle class tends to identify with the rich. They tend to see themselves as hopeful and upwardly-mobile. By getting the working poor to see themselves as having more in common with recent welfare recipients, Obama is hoping to get them to believe that they need/want/are entitled to government help that they might not have sought otherwise, and to form a voting bloc in favor of expanded government redistribution.

Denver Schools Back For More

Posted by Joshua Sharf in Colorado Politics, Denver, Taxes on September 20th, 2012

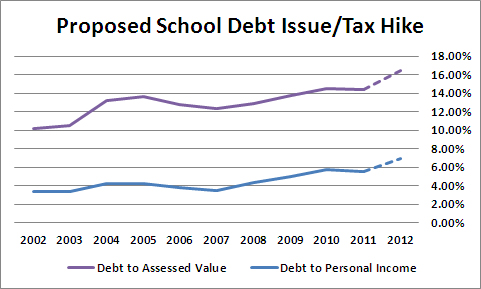

Whenever the schools teachers unions come back for more, they always want you to forget how much they’ve taken in the past. This year, Denver Public School are proposing both a tax hike, and a debt issue. We’ll look at the tax hike another day. What many people don’t realize is that DPS has been borrowing like they had the Fed at the other end of the line (which they sort of did). Over the last 10 years, the bonded debt per capita has almost doubled, and the proposed $466 million increase would, I estimate, raise it almost another $700 per person.

That alone doesn’t tell us much, though, about our ability to pay this debt. The debt is funded through a mill levy on personal property, and is therefore limited based on the total assessed property value in the district.

So to consider how affordable and wise additional debt is, we should look at the ratio of Debt/Assessed Value – in effect, how mortgaged is your property for this debt?

But unless someone annually rolls their property tax into their mortgage, though, they have to pay it out of current income or savings. Which means that it’s also important to consider the debt as a percentage of total personal income. The charts below show how those ratios have risen over the last ten years, with the dashed line estimating how the additional $466 million would increase these ratios:

Both ratios have risen, and would rise dramatically on passage of 3B. Note, though, that the burden on income is rising faster as a percentage basis (vs itself) than the burden on assessed value. The property tax is a regressive tax. While it’s nominally paid by the property owner, they really pass it on their renters, so the burden rests on the entire city. This chart shows that while the debt burden for the school district has been rising as a function of assessed value, it’s been rising even faster in terms of people’s ability to pay.

The DPS and the CEA will always argue that they need the marginal increase. What they won’t tell you is how these marginal increases add up over time.

Note on data sources: The Denver Public Schools, like all Colorado Public School districts, is required to file a Comprehensive Annual Finance Report. It gives the Net Debt for the school district, and also calculates the per capita, and the other ratios. But it only had that data through 2008. While the BEA calculates total personal income at the county level, its latest data was for 2010. The BLS publishes a total wages number at the county level, though, and had numbers through 2011. The ratio of the DPS’s reported total personal income for the county to the BEA number was 1.24, with a standard deviation of 0.02, so I decided to use the BEA numbers multiplied by 1.24 for 2002-2011. With current reports showing wages in Denver declining slightly, and employment static, I plugged in the 2011 number for 2012.

For the 2012 Assessed Valuation, I used the 2011 Assessed Valuation plus 10%, which is about what the Case-Schiller is showing for the Denver area.

For population, I used the official Census estimates for Denver, and then added 16,000 to the 2011 estimate for 2012. These differ somewhat from the population numbers used by DPS.

For the total debt, I simply added the $466 million requested to the latest 2011 Net Debt reported by DPS.

Investing in School…Bonds

Posted by Joshua Sharf in Colorado Politics, Education, Finance, PPC on August 16th, 2012

I’ve written before about the proposed Jefferson County Schools mill levy increase, issues 3A and 3B, which will be on the ballot this fall. The committee supporting the measure is named Citizens for JeffCo Schools (sic), and according to EdNews Colorado (confirmed by TRACER documents), it has raised a little under $50,000 this year. Twenty thousand of that comes from Robert W. Baird, an investment bank based in Wisconsin. Another $15,000 has come from FirstBank, meaning that the remainder of small contributions – under $15,000 – is less than the $15K from FirstBank.

Robert Baird, as it turns out, is the district’s investment banker, confirmed in the minutes of the June 14 School Board meeting (available here). This means that should the bond pass, Baird stands to make a fair amount of money underwriting the refi.

This cycling of money by investment banks back into bond referenda that they stand to benefit materially from is extremely distasteful, and has gotten attention before.

Someone should ask the 3A/3B proponents about this.

UPDATE: Go to JeffCo Students First Action to see what you can do to stop this measure.

How Does PERA Rate?

Posted by Joshua Sharf in Budget, Colorado Politics, Finance, PERA, PPC on August 15th, 2012

Not well. According to its latest Comprehensive Annual Financial Report, PERA has an unfunded liability of $25 billion, up from $15 billion last year, mostly because of a dismal rate of return in 2011, roughly 1.9%. Much of the criticism of public pensions has centered on their unrealistic expected rates of return, 8% in PERA’s case. This is certainly a cause of concern. While 8% is not unrealistic for equities historically, most people consider it to be wildly optimistic, certainly for the near future. And in any case, a constant rate of return doesn’t take into account the volatility of those returns.

But there’s a second rate, the discount rate, which PERA also has to estimate. It signifies something else altogether, and like the discount rate, PERA’s assumptions regarding the discount rate serve to make the fund look more solvent than it actually is.

What is a discount rate?

Another term for the discount rate is the “required rate of return,” not by the plan, but by the investors in the plan. In some sense, you can think of it as the Rate of Return in reverse.

The Rate of Return is used to estimate how much today’s investment will be worth tomorrow. PERA assumes an 8% rate of return, and for the moment, let’s humor them. This means that $1,000 today will be worth almost exactly $10,000 in 30 years.

The discount rate works in reverse. If I know that I’m going to need $10,000 in 30 years, then I can run that number in reverse, discounting by 8% each year, until I see that I need $1,000 in the bank today to be able to meet that obligation.

PERA, like most government pensions, uses the assumed Rate of Return as the Discount Rate. If you have $1,000 in the bank, after all, you have enough to cover a $10,000 obligation.

Why not?

Because in this case, the discount rate is supposed to discount back obligations, not assets. It is suppose to represent the required Rate of Return of the investors, in this case, the pensioners. And since the pensioners’ assets (their PERA benefit) is the same as PERA’s obligations, PERA should use the Rate of Return that pensioners should expect on their investment.

What rate is that? Basic economics says that risk needs to match return. The market should price assets with the same risk at the same Rate of Return. Otherwise, for two assets with the same risk, an investor could sell the one at the lower rate of return, and buy at the higher rate, and not have any risk at all. Obviously that’s not sustainable.

So the trick is to find an investment with roughly the same risk as PERA, and use its return as PERA’s discount rate. PERA is a contractual obligation by the state, much like a long-term bond. It can probably change the terms of PERA more easily than it could default on a long-term bond, but again, let’s assume that these are pretty close to having the same level of contractual obligation, and therefore, from the investors’ point of view, the same risk.

This is what private pensions have to do. A corporate pension would use, as its discount rate, a mix of high-quality corporate debt, because that’s market-traded debt at the same level of obligation as its pension obligation. It’s only by the grace of the Government Accounting Standards Board (GASB), that PERA and other public pensions can get away with the higher discount rate.

Right now, according to MunicipalBonds.com, Colorado has long-term revenue bonds trading between 4,5% and 5%. Conveniently, if we use 4.75%, a $10,000 obligation translates to $2500 today.

So What Does This Mean?

Well, in our example, it shows how the level of fundedness is dependent on the choice of discount rate regardless of whether or not the 8% Rate of Return is realistic. If PERA has $1,000 in stocks, and chooses a discount rate of 8%, it looks as though it’s fully-funded. But if PERA is forced by accounting standards to choose the (more correct) discount rate of 4.75%, it’s underfunded by $1500, and is only 40% funded – even if we can realistically expect 8%.

That’s because the two rates really don’t have anything to do with each other. One is the rate of return PERA expects on its assets from its own investments. The other is the rate of return that pensioners expect on their investment. What PERA invests its money in is a policy decision. It may be good or bad policy, but pensioners expect to be paid, just the same as bondholders do, and that’s what determines the riskiness of the pension as an investment, not whether or not management puts it in gold bars or decides to go to Vegas and put it all on Red.

Ideally, PERA would match its return to its obligations. It would invest at something that also returned 4.75%, and have $2500 in the bank to be able to cover the $10,000 obligation, 30 years from now.

When it’s allowed to select a higher discount rate, though, it can get away with looking fully-funded with a much less money. Obviously, it has every incentive to do that. To do that, it has to seek investments with higher expected return. But in chasing higher returns, it’s also taking on additional risk.

Not only does the higher discount rate make PERA look more solvent than it is. It also encourages it to make riskier investments with its pensioner’s money.

JeffCo Unions on PERA – Watch What We Say, Not What We Do

Posted by Joshua Sharf in Colorado Politics, Education, PPC on August 10th, 2012

This year, Jefferson County Public Schools will be seeking – yet again – a mill levy increase that will reportedly raise $39 million. There are two measures on the ballot: 3A, which will fund operations, and 3B, which will be used to fund capital improvements.

Sheila Atwell, JeffCo parent and president of JeffCo Students First has been leading the opposition to the increase. On July 20, 2012, she and Cindy Stevenson, Jefferson County School Superintendent, debated the measures at the Arvada Chamber of Commerce Leadership Breakfast. During the discussion, Atwell raised the explosive growth of PERA costs to the district over the last few years.

As can be seen in the chart below, Jefferson County is not alone in seeing PERA absorb a greater and greater proportion of its operating budget:

Using reasonable growth rates, Mrs. Atwell projects that within a few years, PERA will eat up 20% – one dollar in five – of Jefferson County’s operating expenses.

Supporters of 3A an 3B have responded that PERA contributions are set at the state level, that neither the county nor the school board have any control over them, and that for that reason, they are irrelevant to the debate over 3A and 3B. Dr. Stevenson had this to say in response to a question about PERA reform at the breakfast:

“As far as PERA goes, it’s a worthy debate to have as a state. We can have that debate. That’s a good thing for a state to debate: how are we going to manage this? But, at the end of the day, we have to pay our share. We are not opposed to reform. Our employees aren’t opposed to refom. But we also have to remember those great starts and strong finishes in the meantime. How are we going to support our kids in their classrooms? And at some point as a state, we’ll untangle this.

“So, yes, it is legislative. Yes, we have to follow the law. Yes, all of those things. But it’s in our budget. We’re gonna pay it no matter what. So, I don’t think PERA is the issue for 3A/3B. It may be an issue, but it is not the issue for 3A/3B.” (Emphasis added.)

Defusing an objection by simultaneously feigning flexibility while maintaining its irrelevance is a classic strategy for dealing with a dangerous issue, and in fact, that’s exactly what Dr. Stevenson is doing here. In fact, both assertions are demonstrably false.

In 2012, four major PERA reform bills were introduced into the legislature:

- SB12-016, which would have given local governments the ability to shift up to 2% of the employer contributions to employees, something the state government can already do

- HB12-1250, which would have tied PERA employer health care contributions to expenses, rather than to employee salaries

- SB12-082, which would have raised the PERA retirement age to that of Social Security

- SB12-119, which would have required PERA to adjust benefits and contributions to keep the amortization period for benefits at or under 30 years

All are moderate measures. None was passed. In fact, none even made it to a floor vote. A lobbyist search shows that each was opposed by some combination of AFT, the AFL-CIO, the CEA, or CASE (the Colorado Association of School Executives). Jefferson County teachers are represented by the JCEA, the county branch of the CEA. The AFT and AFL-CIO jointly run the Colorado Classified School Employees Association, the union for the administrative staff. And CASE presented Dr. Stevenson with its 2010 Superintendent of the Year Award. It’s quite clear that, contrary to Dr. Stevenson’s assertions, JeffCo public school employees – or at least their representatives – are solidly opposed to PERA reform.

As for the Board itself, the unions have been active in school board races for at least that several cycles. A TRACER search reveals that two of the Board members, Paula Noonan and Jill Fellman, received considerable union financial assistance in their election campaigns, while Linda Dahlkemper is the wife of former Congressional candidate Mike Feeley, so was evidently well-connected on her own, and able to raise enough money from the Democratic establishment. (In fact, a number of current and former Democrat officeholders were prominent contributors to her campaign.) And the union contributed several thousand dollars to the losing 2009 campaign of Sue Marinelli. It would be unreasonable to expect board members, some of whom likely hold their seats as a result of union support, to support reforms so strongly opposed by their campaign benefactors.

It is the height of disingenuousness to claim that the solution to PERA is at the state level, and to claim that the district has no flexibility in dealing with it, and then to oppose those very reforms, including one that would have explicitly given the Board the very flexibility it says it doesn’t have. (In fact, the Board and the unions are always at liberty to negotiate changes to the employer-employee contribution mix.)

Dr. Stevenson claims that because of that inflexibility, PERA contributions are set by the state, so 3A& 3B are irrelevant. However, the reason that JeffCo is pursuing a mill levy increase this year is that in December, the district finished paying off a bond issue, and the Board wants to hold onto that revenue stream, so that it doesn’t have to come back to the voters and ask for the entire mill levy increase. Instead, it can apply the existing bond mill levy to the proposed increase, making the apparent increase smaller. In theory, a mill levy dedicated to debt can only be used for other debt, once the initial bond is paid off. In reality:

“What [those proposing the increase] realized was we had a unique opportunity right now to get money into our classrooms for great teachers, great education, and not increase your property taxes to an extreme level. Here’s why we have that opportunity. We are going to be paying off bonds in December, that’s true. That equals about 4.75 mills. Now, there’s nothing in statute that says the Board has to refund that. We can do that, or we can apply it to other debt. Sheila is right: you can’t move bond mills – that’s the way I think about it – to operations. However, we can look at the total mill increase.” (Emphasis added.)

Dr. Stevenson all but admits that the right way to think about the JeffCO school budget – any budget, in fact – is to consider it as a whole. Money not used for debt reduction can be applied to operations. Or PERA.

Whenever a government asks for a tax increase, it’s sold on the basis of things like “great starts and strong finishes,” but much of the time, ends up going to feather the nest of those proposing it. Mrs. Atwell has correctly identified the source of a large and growing structural gap in JeffCo’s school financing, one which ought to be addressed before asking the public to turn over more money to the district.

UPDATE: Go to JeffCo Students First Action to see what you can do to stop this measure.

Denver Mayor Michael Hancock’s Lack of Vision

Posted by Joshua Sharf in Colorado Politics, Denver, PPC, Taxes on August 3rd, 2012

The following is a Guest Commentary published this morning in the Denver Post. For the uninitiated, since 1992, Colorado has had a law on the books called TABOR, or the “Taxpayers Bill of Rights.” The bane of tax-raising legislators statewide, it limits revenue growth to inflation + population, year over year. In the case of cities, this means that a city may only be entitled to keep a portion of the mill levy on a property’s assessed value, returning the rest to taxpayers. TABOR includes a provision known as “De-Brucing,” after TABOR author Douglas Bruce, whereby the residents of a district may opt out of those limitations, and allow the city to keep the full mill levy on the entire assessed value of a piece of property. To date, Denver has not done so, and this year, Mayor Michael Hancock is proposing that the City Council approve a referendum for Denver citizens to do just that.

At the invitation of the Independence Institute, I wrote the following piece, opposing the proposed tax measure:

UPDATE: The Post edited the piece somewhat for space. An earlier version of this post just used what they printed. I’m replacing it here with the slightly longer version that was submitted to them.

Denver’s a big city, a major element of Colorado’s economy, and of the Rocky Mountain West. And its governance is not for the faint of heart. But the Hancock Administration is not asking the hard questions, Instead the administration is seeking the easy way out of a budget deficit through a proposed permanent property tax increase for the November ballot.

Instead of proposing bold changes to Denver’s fiscal structure, Mayor Hancock has opted to tinker around the edges of city finances, and stick Denver homeowners with the bill for his lack of vision.

Denver is just beginning to recover some of its housing value. Yet, only a month ago, the Denver Post reported that “another wave of foreclosures appears to be looming.” A sudden increase in property taxes strikes at the heart of households’ precarious financial stability, even as government take a bigger bite of homeowners’ slowly increasing equity. Renters would also be affected, as property owners pass along the increased expense.

The mayor’s proposal assumes that rising home values necessarily mean rising incomes. But the Bureau of Labor Statistics reports Denver’s weekly income fell nearly 5% in 2011, 305th out of 323 major counties surveyed. The mayor’s mill levy override scheme would mean an immediate property tax increase of 20% for households who are still finding it difficult to make ends meet.

Denver’s unemployment rate remains stubbornly high, at 8.7%. The Mayor’s Structural Financial Task Force cites a failure to create jobs as one reason for lower revenues. That’s hardly a reason to penalize the employed and unemployed alike.

Another of the mayor’s proposals, eliminating the business personal property tax for new purchases, is a smart and welcome revenue enhancing move, but merely shifting the tax burden from struggling business owners to struggling families – often the same people – will leave us no better off.

When the government proposes a tax increase, it’s claiming that the least important thing it can do with that money is more important than the most important thing you can do with it.

Many households’ finances are just beginning to stabilize after years of uncertain employment. People have savings to rebuild, retirements to plan for, and children to feed, clothe, and put through school. Maybe even take the odd vacation they’ve been putting off for years.

The government has a moral obligation to exhaust all reasonable efforts at cost savings before asking taxpayers for more. But the mayor hasn’t just “gone small” on savings, he’s also “gone vague.” With the exception of specific personnel moves, the overwhelming proportion of savings includes studies and promises to find cost savings, rather than actual cost savings.

The mayor’s proposals to increase retail sales and identify unused parcels of land assume that private developers are incapable of doing this themselves. At a recent hearing on the redevelopment of the old Health Care District near 9th Ave. & Colorado Blvd., the developers identified that parcel as one of the most desirable retail spaces in Colorado.

The mayor’s rejection of specific fees for libraries and trash collection may avoid taxpayer ire, but it’s hard to escape the feeling that the decision had more to do with avoiding the accountability imposed by earmarked revenues.

Genuinely bold proposals would include privatizing or outsourcing such city services as vehicle fleet maintenance, building and road maintenance, and park maintenance and rec centers.

Big city Democrat mayors have championed similar moves across the country, including Rahm Emanual in Chicago, Antonio Villaraigosa in Los Angeles and Alvin Brown in Jacksonville. Newark Mayor Cory Booker has been at the helm of an astonishing and ongoing turnaround of that troubled city. Facing a fiscal crisis during his first term, Mayor Hickenlooper made ends meet without resorting to tax increases. One reason he became governor was his understanding that Colorado has “no appetite” for tax increases.

In California, where cities like Stockton and San Bernardino have declared bankruptcy due in part to crushing public pension obligations, voters in San Diego and San Jose voted overwhelmingly to significantly reform public employee pension and health plans.

Earlier this year Newark’s Mayor Booker was the featured speaker at the Colorado Democrats’ Jefferson-Jackson Day Dinner. While he spoke largely about his personal story, he no doubt talked city business with Mayor Hancock privately during his visit.

Unfortunately for the citizens of Denver, Mayor Hancock’s proposed permanent property tax increase for the November ballot shows that he wasn’t listening.

Denver voters should recognize this proposal for the lost opportunity that it is, and instruct their leaders to try again.

About That Battleground States Poll

Posted by Joshua Sharf in 2012 Presidential Race, Media Bias, PPC, President 2012 on August 1st, 2012

The MSM is making much of this morning’s Quinnipiac/NY Times/CBS poll allegedly showing President Obama moving ahead in the battleground states of Ohio, Pennsylvania, and Florida. This poll should carry more weight, since it is a poll of likely voters, probably identified by whether or not they voted last time, and whether or not they voted in the primary. But as is often the case with MSM polls, the internals belie the conclusions.

The poll shows President Obama leading Governor Romney 50-44 in Ohio, 53-42 in Pennsylvania, and 51-45 in Florida.

Obama actually won these states 51-47, 54-44, and 51-48, respectively. That in itself should raise some suspicion. I don’t know of any other significant polls that show Obama running ahead of where he did in 2008. Nationally, he won by 7 points, and Rasmussen’s daily likely-voter poll has shown only occasional movement from a 47-44 Romney advantage. I suppose it’s possible that concentrated saturation-bombing could move polls in individual states, but I’ve seen such tactical strategies in the past, and they almost always come from losing campaigns.

The other odd number is how people claim to have voted in 2008. These are, respectively, 53-38, 54-40, and 53-40, or +11, +4, and +10 vs. how those states actually went. Even assuming people moved around, the numbers for Ohio and Florida are huge, and the number for Pennsylvania is still significant. While people are more likely to remember themselves as having voted either for a winner, or for their current preference, even if they voted the other way, it’s hard to believe these are representative of the people likely to vote in this election.

Lord knows, I’ve been wrong about polls before. Tomorrow morning at Denver’s First Thursday Breakfast, pollster Floyd Ciruli – a Democrat, but you’d never know his party affiliation from his commentaries – will be speaking. I’ll ask him about these conjectures then, and report what he has to say.

Children of the Corn

Posted by Joshua Sharf in Business, Colorado Politics, Economics, Energy, PPC on July 27th, 2012

My latest for Who Said You Said:

“When everyone says you’re drunk, you’d better sit down.” When both The Wall Street Journal and NPR have questions about a policy, it’s time to rethink it.

The Renewable Fuel Standard’s ethanol mandate requires an increasing amount of ethanol be blended in gasoline every year. Last year, more than a third of America’s corn crop went to ethanol; this year, with decreased production and increased diversion, that proportion is expected to rise to at least 40%. This requirement has pitted ethanol producers against food and feed consumers of corn, driving up corn prices even faster than normal supply shortages would dictate.

The EPA could, if it chose, suspend the ethanol mandate altogether for the year, but so far has chosen not to do so. Not only Agriculture Secretary Tom Vilsack, but Interior Secretary Ken Salazar have been strong supporters of ethanol. On July 16, 2008, Salazar, then a U.S. Senator from Colorado, spoke on the floor of the Senate in terms of ethanol’s contribution to America’s “energy independence,” its importance in keeping gas prices down, and the jobs that were then being created on Colorado’s eastern plains in the new ethanol plants being opened there.

The Obama Administration may have been caught off guard by the severity of the current drought, but questions about price distortions caused by the mandate aren’t new. Last year, in February of 2011, Vilsack addressed exactly these same concerns at a press conference [See CNSNews.com video above]:

“Certainly not worried in the long term about our capacity to produce enough corn to meet our food and feed needs as well as our fuel needs. The last time we had any issue relative to food prices when this issue was raised about ethanol production, our studies indicated that the ethanol production was a very, very, very small percentage of the food price increases.

“When you look at food price increases, you’re looking more at marketing, advertising, refrigeration, transportation, expenses that are incurred in the food chain. And you’re also recognizing that farmers are receiving an ever shrinking share of the retail food dollar. There are a lot of folks that have to be satisfied out of that retail dollar.

“So I’m not concerned about it. We obviously will continue to look at what the Spring will bring, in terms of cropping decisions. Part of what’s happening worldwide is the result of weather conditions in a number of countries. Export controls and restrictions by some countries have made it a little more difficult. But here in this United States, we’re anticipating food prices to rise somewhere between 2-3%, which is relatively moderate.”

The problem, of course, is that neither people nor livestock can wait for the long run to eat. It may be easy enough for us to adjust to some food price increases, but folks living closer to the margin, as in Mexico, don’t have that luxury. See Egypt for what happens when entire countries have to choose between food and fuel.

And while Vilsack has correctly identified the price inputs into food production, he’s forgotten that prices change because of action on the margin, and the price of corn has proven to be especially volatile, but also especially remunerative to farmers in recent years. A large part of this increase is a result of the ethanol mandate. And contrary to Sec. Vilsack’s protestations that little of the money is flowing through to farmers, agricultural land values have been shooting through the roof, indicating that investors see corn production as a good investment.

The winners include ethanol producers, who are guaranteed a market for their product, corn farmers, who see the results of the government bidding against private ranchers and farmers for their product, and fertilizer companies, whose nitrogen-based product is needed to save the soil from the increased corn crop. Much of the increased corn planting takes place at the expense of soybeans, which replenish the soil. (As a side note, a major component of fertilizer is natural gas; the combination of falling natural gas prices and rising corn plantings has been a windfall for those companies, so to the extent that the farm vote is in play, look for politicians to make hay with that.)

The losers include ranchers, who are having to bid against the government for corn to feed their herds, and you. Because not only are food prices rising faster than your paycheck, there’s little to no statistical evidence that all this diversion of food to fuel is keeping gas prices down. And in spite of the mandates, ethanol plants are shutting down, anyway.

For decades, as their agriculture became a running joke, the Soviet Union used to blame chronic food shortages and poor crops on the weather. A Russian history professor of mine responded to a student’s question about Gorbachev’s political prospects, “Well, he’s got his main rival (Yeltsin) in charge of agriculture, so I’d say he’s in pretty good shape.”

It’s doubtful that Barack Obama felt threatened by Vilsack’s presidential ambitions (his abortive presidential run ended in early 2007, about a year before his home-state Iowa Caucuses), but it’s likely that Vilsack will end up as collateral damage of this Administration’s misbegotten economic and energy policies, nevertheless, when he finds himself – hopefully – looking for work after the November elections.

JeffCo’s Teachers Unions Shell Game

Posted by Joshua Sharf in Colorado Politics, Education, PPC on July 23rd, 2012

Another year, another school bond issue. This year, it’s Jefferson County where Referenda 3A & 3B will be on the ballot, asking property owners to increase the mill levy. 3A will fund operations, 3B capital investment.

The unions favoring the increase are using the usual scare tactics, of course. But this year, thanks to Sheila Atwell at Jeffco Students First (among others), they’re having to play defense on a number of issues, including the district’s PERA contributions.

The union claims, with some truth, that:

PERA contribution rates also cannot be changed through this November’s mill and bondelection. Money from 3A supports local schools and prevents further cuts to instruction; money from 3B goes to badly-needed maintenance and repair on the schools. Money from 3A and 3B does not go to PERA.

Currently, it is not possible for the Jeffco Board of Education to ask district employees to pay a higher percentage of their own PERA contributions to offset budget shortfalls. Senate Bill 11-074 was introduced in February 2011 and would have allowed school districts like Jeffco to raise the employee contribution rate and lower the employer rate, but that bill died in committee. No new legislation has been presented since 2011.

Because no new legislation has been introduced since 2011, changes made to PERA contribution rates can only made through legislation by the Colorado General Assembly at the state capitol.

Others have suggested that PERA is a union issue. It is not. Unions cannot change the state-mandated rates. PERA is a state issue and citizens who want to see it changed need to lobby their state representatives to do so.

Mixed in with the truth, however, is a healthy helping of disingenuousness. They are correct to this extent: The specifics of PERA are set by the legislature, and are not really negotiable at the local level.

That’s about where it ends. That PERA contributions are fixed, doesn’t mean that they don’t exist. They are a very real – and growing – part of the school budget. By taking that off the table for discussion, the CEA is asking homeowners – all taxpayers, really – to work harder and longer to fund union members’ retirements, while putting off their own.

The Democrats in the state legislature did indeed kill a bill, SB11-074, that would have permitted localities and school districts to shift some of the PERA contributions from employer to employee, as the state can do. A quick search of the Secretary of State’s site shows that among those instructing their lobbyists to oppose SB11-074 were PERA itself, the Colorado AFL-CIO, and the CEA.

To use the fact that the structure is set by the legislature as an excuse to persuade taxpayers to raise their own taxes for your benefit, advise them to seek redress at the Capitol if they don’t like it, and then actively work to frustrate that reform, is the kind of tactic that might have worked once, before the Age of Transparency, but no longer.

There was a 3% reduction in pay, but there’s no reason to attribute that specifically to PERA, to call it the teachers’ contribution to PERA solvency, as the union tries to do elsewhere on the page. What they want to do is to day that taxes aren’t going to PERA, while their pay decreases are. It’s the same sort of rhetorical shell game that unions often play.

The Bureau of Labor Statistics quarterly survey of wages shows that the average weekly JeffCO wage declined by 3.9% year-over-year in QA of 2011. So it’s all in the spirit of shared sacrifice.

UPDATE: Go to JeffCo Students First Action to see what you can do to stop this measure.

-

You are currently browsing the archives for the Colorado Politics category.