Archive for April 18th, 2010

Inflation and Gold

Posted by Joshua Sharf in Economics, Finance on April 18th, 2010

Gold fanatics are of the opinion that the gold markets are predicting a massive run-up in inflation. Their policy responses run from abandoning the Fed, to establishing competing currencies, to establishing gold as legal tender for debts, and are not mutually exclusive. The problem is, the debt markets tell another story.

Since 2003, the US Treasury has offered 10-year TIPS, Treasury Inflation-Protected Securities, bills whose coupons is linked to inflation. At a fairly simplistic level, but an internally consistent one, you can subtract the TIPS rate from the nominal 10-year Treasury rate to see how the markets are pricing 10-year inflation:

As you can see, from mid 2003 until late 2008, the market pretty consistently priced inflation at about 2.5%, and that’s about where it was most of the time. Then, in late 2008, the world came to and end, and with the 2nd Great Contraction, the TIPS rate jumped up to the nominal rate, indicating that inflation was the least of anyone’s concern. The last 16 months have seen a gradual return to historical averages for inflation. But even as nominal rates have risen, the TIPS rates have kept pace, and the current implied inflation, 2.33% is at or slightly below historical averages.

Compare this to gold over the last few decades. Here’s just over 40 years’ worth of gold price info: the current price, the CPI-adjusted price, and the CPI (1982=100):

So much for gold as an infallible inflation hedge. From 1983, prices march inexorably upwards, but I’ll wait until 2010 for the real price of gold to come back. The quadrupling of gold’s real price from 1970 to 1975 doesn’t seem justified by the CPI, and while there’s a definite bump in the CPI in 1980, again, it doesn’t seem to justify gold’s move from $200 to $800. Then, even as there’s another little bump in 1990, gold prices continue down.

Gold is a commodity, with its own price dynamic. Fear can drive up the price, and people move to safety. But gold can also be its own bubble, with inflation being the justification rather than the cause. Like any other commodity, there’s supply and demand. Gold bugs tend to focus on demand. But…

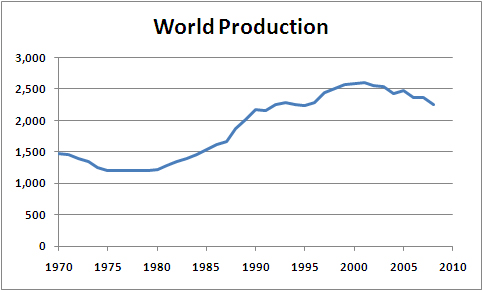

This is the world production of gold according to the USGS. Now, we’ve seen declines in the production of gold before, so perhaps this isn’t “Peak Gold.” In the early 1970s, coinciding with the run-up in prices from ’72-’75. After 1980, production picks up in response to the bubble, and continues to rise until 1990 or so. And then, from 1996 until 2010, production and price are almost inverse to each other.

If this is Peak Gold, if new veins aren’t as productive, and worldwide production will continue to fall, then that goes a long way towards explaining the recent run-up.

This doesn’t mean that inflation won’t happen, or that all’s right with the world. The massive pile-up in federal debt is the sort of thing monetary catastrophe is made of. And once a loss of confidence occurs, it usually happens more swiftly than imagined, even by most who expect it. The credit markets can, and do, miss signals. Perhaps they’re pricing in a higher likelihood of either default or punitive tax rates to make up for the unbearable entitlements we’ve loaded onto ourselves. Or perhaps, more ominously, they’re just not looking beyond the next couple of years, and since we can’t predict when the bottom falls out, there’s no point in trying.

But gold bugs can’t pick and choose signals, and right now, the credit markets just aren’t signaling, “Weimar 1923.” A comprehensive theory has to encompass all the data. The simplest answer is that the run-up in gold isn’t very much about inflation, but about simple supply and demand, with supply falling as much as demand picking up.

-

You are currently browsing the archives for Sunday, April 18th, 2010