Archive for category Regulation

Greeks Bearing Grifts

Posted by Joshua Sharf in Business, Economics, Finance, PPC, Regulation on June 16th, 2011

And if the threat of starvation and a southern land rush weren’t enough here on Disaster Wednesday, there’s always Greece:

…But conditions in European markets are deteriorating. The main risk from Greece has always been contagion, and that process is already under way.

Most directly, prices of Portuguese and Irish bonds have fallen sharply, with 10-year yields rising above 11% and the cost of insuring their debt at record levels. The gap between Spanish and German 10-year bond yields is at its widest since January. The market is effectively giving no credit for any reforms or budget policies set out in the past six months.

The next link in the chain, the banking system, has been affected. In Spain, progress by banks on regaining market access has gone into reverse: Average borrowing from the European Central Bank jumped to €53 billion ($76.32 billion) in May from €42 billion in April.

Meanwhile, the contagion into core banks may be being underestimated by investors. Moody’s on Tuesday said it could downgrade France’s BNP Paribas, Société Générale and Crédit Agricole due to their holdings of Greek debt, and the ratings firm is looking at whether other banks could face similar risks.

Disturbingly, the worries have now reached non-financial companies, which have been virtually bulletproof this year. Investment-grade bond issuance has come to a near-standstill.

I seem to remember having seen this movie before, as the prequel to to 2008’s Episode IV: A New Hope. It may provide some cold comfort to Americans that this time, it’s taking place in Austrian, even if Germany’s pending LBO of the rest of Europe isn’t the Teutonic Shift the President had in mind a couple of weeks ago.

But there’s no particular reason to be complacent. Just as we’ve managed to convert our economy from fast-falling to encased-in-amber stasis, we could be in for another financial shock. Megan McArdle suggests one route: (I hate to quote a post in almost its entirety, but it’s short, and I don’t think I can say it better)

During the wave of banking regulation that followed the Great Depression, the government slapped heavy controls on the interest rates that banks could offer. They weren’t very good, which made the banks sounder, and consumers worse off. When inflation and interest rates rose in the late sixties, this became a big problem. Then some clever chap came up with the money market fund. Legally it worked like an investment fund, not a bank account: you invested in shares, with each share priced at a dollar. The fund invested in the commercial paper market and committed to keep each share worth exactly one dollar; whatever investment return they got was paid out as interest on your shares. This gave you something that looked a lot like a bank account, without all the legal tsuris.

In 2008, it turns out that these money market accounts were–as was always pretty obvious–a lot more like bank accounts than mutual fund shares. The Reserve Primary fund held a lot of Lehmann Brothers commercial paper, which plunged close to zero, meaning that there were no longer enough assets in the fund to make all the shares worth at least a dollar. This is known as “breaking the buck”, and it was not the first time it had happened. But it was the first time in more than a decade that it had happened at a fund which didn’t have enough money to top up the assets in the fund to bring them back to a value of $1. Bigger investment houses had been quietly topping up their money market funds for month, but Reserve Primary was a smaller firm, and they didn’t have the spare cash handy.This triggered a run on the money markets, which the government really only stopped by a) passing TARP and b) guaranteeing money market funds. But as Matt Yglesias points out, Dodd-Frank stripped Treasury of the authority to do such a thing again. And now the money markets are exposed to a Greek default.

Something like 45% of US Money Market funds have some direct exposure to Greek debt. Greece defaults, and many of these funds may be breaking the buck without Big Ben backstopping for them.

But that’s only the direct exposure. Then, there’s the indirect exposure, though insurance, and (probably) Credit Default Swaps:

Finally, it’s worth noting that once you account for the substantial payouts that US agents will have to make to European creditors in the case of a default by one of the PIGs, financial institutions in the US have roughly as much to lose from default as those in France and Germany. (See the figures in blue in the table above.) The apparent eagerness of US banks and insurance companies to sell default insurance to European creditors means that they will now have to substantially share in the pain inflicted by a PIG default.

The risk to US banks itself may be small, but the effects of having sold this insurance, and of people finding out that they sold this insurance, could be substantial:

The big US banks are well-capitalized now, and can fairly easily absorb losses of several billions of dollars in the event of a Greek default. But two serious concerns remain. First, I fear that this may have the potential consequence of exacerbating the flight to safety that will happen in the event of Greece’s default; if you have no idea who is really going to be on the hook and ultimately liable for CDS payments, your best strategy may be to trust no one. I don’t think that triggering post-traumatic flashbacks of the fall of 2008 is going to do good things to the market or the economy. Second, I wonder if there’s a public relations disaster just lying in wait for the big US banks. After all, how will you feel (assuming you don’t work on Wall Street) when you read the headline that Big Bank X lost money because it sold billions of dollars of credit default insurance while it was on taxpayer life-support? Rightly or wrongly, I’m guessing that Big Bank X will not be very popular for a while.

This also doesn’t address the US banks’ exposure to the European banks, the ones that may go under when Greece finally decides to call it quits. They may have positive exposure to those banks, and find that holdings in them, or loans to them, are suddenly less liquid than they had hoped.

There’s one other issue that I haven’t see addressed anywhere, and that’s the question of securitized Greek debt. Remember that we thought the subprime crisis could be “contained,” because subprime mortgages were such a small portion of the overall mortgage market, never mind the credit markets as a whole. Then it turned out that the subprime assets were poisoning entire classes of securities, since they were so highly leveraged. Is it possible – and this is purely speculation, I really do not know the answer to this – it is possible that people have done the same thing with sovereign debt, and that there are CDOs out there with Greek debt incorporated into them? Securities that could suddenly default, even though they only contain a small mix of drachmas in there?

Carmen Reinhart and Ken Rogoff point out that after every financial crisis, governments find themselves with significantly higher debt, as they seek to stop the dominoes from falling. The potential exists for European governments to become dominoes themselves, and if McArdle is right, there’s some risk (probably small, but hard to say how much) that won’t even be able to step in again and keep our own house in order.

Ethanol and Natural Gas

Posted by Joshua Sharf in Business, Economics, Energy, PPC, Regulation on March 30th, 2011

UPDATE: And as if on cue, this morning, JJG, Barclays ETF on grains, is up almost 5% this morning. This is not just a generalized inflation play (meaning this isn’t just about the Fed printing dollars), since GLD and TBT (the bearish bet on the 10-year Treasury) are up, but only about 1%.

Much has been said about the contradictions between the energy policy that President Obama announced today, and how his government has behaved up until this point. But even taken on its own terms, today’s ethanol-and-natural-gas announcement contains enough internal contradictions to make it fall over like a basketball player with his shoes tied together.

The key point here is that ethanol already depends heavily on natural gas. Twice. Directly, as an ingredient in its production. But ethanol is made from corn, and corn – especially when planted in the same fields, year after year – requires a lot of fertilizer. And the key component in ammonia-based fertilizers like anhydrous ammonia, urea, and ammonium nitrate in nitrogen. From natural gas.

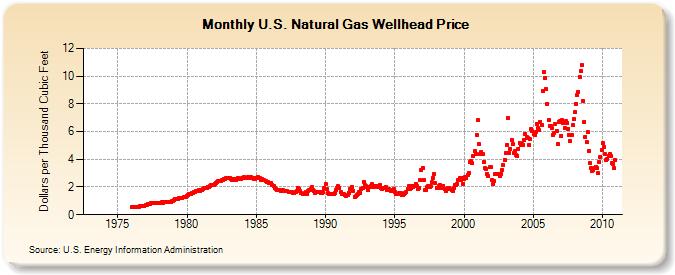

When I worked at the brokerage, one of the companies we covered was a fertilizer company (since bought out), based in the heart of the corn belt. We considered it an ethanol play, with the company remaining profitable as long as corn plantings increased and natural gas didn’t get too expensive. Again. Here’s the chart for the wellhead price of US natural gas:

In 2007, during the last burst, corn planting came at the expense of soybeans, which returns nitrogen to the soil. This meant a large increase in the amount of fertilizer necessary. For the last few years, soybean planting has returned to its long-term trendline, and increased corn production appears to have occurred at the expense of winter wheat, which uses a comparable amount of fertilizer:

Up until now, that’s meant that increased corn plantings, inadequate though they may be, haven’t in and of themselves driven up the price of natural gas. This year, however, soybean plantings may be down, as corn nears its postwar high, meaning additional natural gas demand.

All of this is happening even without Obama’s intervention to commandeer even more of our food for fuel. We already push 1/3 (yes, one third) of our corn harvest into ethanol plants rather than kitchen tables, which amounts to about 8% of the world supply of corn. Any additional ethanol subsidies will only make things worse.

Moreover, Obama’s plan does absolutely nothing to increase natural gas production. To do that, he seems satisfied to ride herd on oil and gas companies that already have more than enough incentive to increase production, if only our government would let them. (Sadly, Colorado, between Ken Salazar and Diana DeGette, is playing a disproportionate role in enforcing that dictate.) He does, however, propose all sorts of subsidies to encourage increased natural gas consumption, promising to drive the price up even farther.

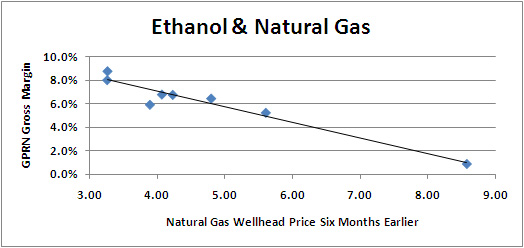

To circle back to my original point, this is going to make ethanol unprofitable even with subsidies. Just for fun, I went back and looked at the gross profit margin for Green Plains (GPRE), a major ethanol producer, and compared it to the natural gas price six months earlier, for the last 8 quarters:

The correlation is an astounding -0.96, which is about as close to metaphysical certainty as you get in statistical analysis. Those who know something about statistics will say that the outlier increases the correlation, and they would be right. If we get rid of the outlier, the correlation is still -0.84, and the slope of the line only changes slightly. If the other points, the ones below 6.00 on the price scale, were clustered together, that would be a problem. But they lie on a nice line of their own.

Using a very rough model, using the company projections for unit sales over the next year, assuming that interest rates don’t rise and the company doesn’t take on any additional debt, the wellhead price of NG would have to rise to 6.8 to eliminate the company’s pre-tax earnings completely for the next year. That’s happened twice over last decade, and this administration’s policies will only make it more likely. Let that happen, or interest rates rise, or both, and see how fast Green Plains decides that it really does need those subsidies – and more – after all.

To the extent that ethanol production can increase, it will help drive up natural gas prices. To the extent that it can’t, its price will rise, and it will need compete for ever-more-scarce natural gas.

Even if ethanol weren’t already a colossal waste of money and resources, this plan couldn’t be designed any better to make things worse.

In this at least, Obama’s being consistent with the rest of his economic policies.

Keep On Truckin’

Posted by Joshua Sharf in Business, Energy, PPC, Regulation, Transportation on March 21st, 2011

That was one of the less forgettable catch-phrases from the 70s, when the independent trucker seemed to embody what remained of the free spirit of America. The part, anyway, that was engaged in constructive work rather than the self-indulgent self-destructiveness that came to pass for independence during that decade.

In fact, trucking has become increasingly regulated over the years, so much so that the notion of the independent trucker, gamely staying awake to deliver his load, is a thing of the past. And with good reason. These are very large, very dangerous vehicles. They’re necessary, but they share the road with, and occasionally crush, passenger vehicles a fraction of their size and weight. As a result of making sure that drivers get a decent amount of rest, the number of fatalities involving heavy trucks, per 100 million miles traveled, was at 2.34 in 2005, down from 6.15 in 1979. More recent analyses have it falling even farther. And those same statistics show truck driver fatigue as a factor in only 1.7% of those crashes. The accident rates continue to decline.

So naturally, what we need is: more rest time!

That’s right. The government has proposed rules that will require longer rest times, fewer hours on the job, more frequent breaks. At first, this sounds like something truckers might like. Until you realize that it’s basically forced idleness, with little marginal benefit to the rest of us using the roads. Truckers hate sitting around. They have loads to deliver, and a forced 15-minute break is actually more stressful, because instead of taking the break when the need it, they’re just as likely to be sitting around watching the clock tick until they can get back on the road.

The company that I am currently contracting for, Werner Enterprises, ran a little experiment with one of their more seasoned drivers, asking him to work to the rule for a month to see what would happen. Turns out that idle trucks aren’t just the Devil’s workshop, they’re also expensive. Two-day trips stretched into three days, and his income, which is based on miles covered, dropped 6% year-over-year. Adopted nationwide, these standards would not only play havoc with the many businesses that use just-in-time inventory management, they would amount to a pay cut for the drivers they’re supposed to help. And in an industry that tends to face driver shortages in good times, anyway, it would require even more drivers, and even more trucks, with all of the overhead that implies, even before they drive their first mile.

This is not an industry that opposes regulation for opposition’s sake. They ended up supporting, for instance, the stricter rules against cell phone use. There are signs on many of the tables in the company cafeteria warning truckers against cell phone use, not on the grounds that if they get caught, they’ll lose their commercial license and have to hitchhike back home from Keokuk, but because it’s dangerous.

They object to this brilliant idea, cordoning off I-70 at certain hours, because it would greatly complicate route planning, on a fairly major truck thoroughfare. (C’mon guys, just widen the road, already.) In combination with the new rules, mandating stops where it might or might not be possible to stop, it would turn driving that stretch into a nightmare.

Colorado’s own Cory Gardner serves on the House Energy and Commerce Committee, which might be able to exercise some oversight here. (Although, so does Diana DeGette, who’s probably miffed that even after decades of trying, there are still trucks on the road at all.) Perhaps he can take a look at this.

Selling The Cure For The Disease They’ve Caused

Posted by Joshua Sharf in Business, Economics, Health Care, PPC, Regulation on January 23rd, 2011

According to the New York Times, the federal government, apparently unhappy with drug companies’ productivity in the last 15 years, has decided to go into business for itself:

The Obama administration has become so concerned about the slowing pace of new drugs coming out of the pharmaceutical industry that officials have decided to start a billion-dollar government drug development center to help create medicines.

The new effort comes as many large drug makers, unable to find enough new drugs, are paring back research. Promising discoveries in illnesses like depression and Parkinson’s that once would have led to clinical trials are instead going unexplored because companies have neither the will nor the resources to undertake the effort.

The Times then goes on to note that, “drug companies have typically spent twice as much on marketing as on research, a business model that is increasingly suspect.” NIH has long been involved in basic research, but this is the first time that the government will get into the business of actually developing and conducting clinical trials of drugs.

We’ll dwell for a moment – but only for a moment – on the Times’s, and by implication, the Administration’s, utter neglect of the possibility that the FDA’s culture of risk-aversion, insistence on testing for efficacy (as opposed to just safety), and the WTO’s failure to protect intellectual property have all contributed to a risk-aversion on the part of the drug companies.

But there may be something else going on here, too. It’s entirely possible that we’re seeing a short-term phenomenon that’s being mistaken – or portrayed – as a long-term one. In, City Journal (“Hooray for Blockbuster Drugs“), Paul Howard argues that the development of incremental improvements is a good thing. for a variety of reasons. It’s certainly something that the regulatory regime encourages. But aside from that, it’s the logical filling-out of major advances that came very quickly, based on basic research that was done much earlier.

Eventually, the diminishing returns from this sort of thing, and the increasing costs and uncertain returns of marketing them, should lead one or more major drug companies to take the leap and try to productize some of the results of gene-based research. The first efforts are likely to be more risky and more expensive, and our current policies have probably exacerbated a reluctance to take large risks in a down economy by raising those costs, both certain and uncertain.

The worst part? Paul Howard:

Some of these investments have been overhyped, but others will eventually produce breakthrough innovations, just as the investments of the sixties and seventies did. And when they do emerge, new technologies (including much more sophisticated diagnostics) will allow doctors to choose drugs for patients most likely to benefit from them. The advent of personalized medicine will also give companies powerful new marketing and pricing leverage. The size of the market for particular drugs may shrink—and drug companies may become smaller and more nimble to exploit fast-moving scientific discoveries—but insurers and governments will find it much more difficult to ration access to targeted therapies. (Emphasis added.)

Just at the time when the new drugs have the chance to democratize medicine in a way that the Internet has democratized political debate, the government is going to step in and make sure that doesn’t happen.

The $1 billion committed to the project so far is about 2% of what drug companies already spend on R&D. It’s hard to believe that this is a better answer than lowering regulatory costs and uncertainties.

The Revolution Eats Its Own

Posted by Joshua Sharf in Business, China, Economics, PPC, Regulation on January 23rd, 2011

We may have to wait a little longer to start breaking China’s stranglehold on the world’s supply of rare earth metals. Something called the Western Watersheds Project has filed a lawsuit to derail a solar project in San Bernadino County, and that same lawsuit may have the effect of shutting down a spur from an existing gas pipeline that Molycorp will need to power its mine. The offended species? Tortoises.

Concerning Molycorp, Connor pointed to an 8.6-mile pipeline proposed to carry natural gas to Mountain Pass for power generation. The so-called Mountain Pass Lateral will, if allowed, carry gas from an existing line owned by Kern River Gas Transmission Line near the Ivanpah Solar Project. “The lateral will pass by the Ivanpah Power Plant, the area where the tortoises are to be relocated, Connor said. “They were given no consideration.”

George Kenline, San Bernardino County’s mining geologist, who issues mining permits and other relevant county permits, praises Molycorp’s new direction. Once a major polluter, Molycorp, he said, “It (Molycorp) decreases the amount of impact because it eliminated the evaporation ponds,” which were a major problem before and have been completely removed from the new project.

Ironies about, the most obvious of which is the attack on a solar project by an environmental group. But then, there’s the fact that the Watersheds Project is seeking to derail a mining operation that has completely changed the way in which is uses water, recycling almost all of its water and getting rid of evaporation ponds. As well as the fact that the rare earths are used extensively in high-power magnets in hybrid vehicles, electric vehicles, and wind turbines. Environmental groups, which enjoy specially-granted standing to file these sorts of suits, are now standing in the way of the kind of change they claim will save us all from catastrophe. Revolutions do eat their own, after all.

Molycorp may have the permits to operate the mine, but it can’t do so without natural gas. It’s further evidence that while a strategic stockpile of rare earths might be a good idea, the real solution is clearing away the regulatory underbrush that ties down useful projects in the first place.

In the meantime, engineers are trying to create high-power magnets that don’t use rare earths at all. This is equally big news in the longer-term, but for the moment, as in so many other similar efforts, the problem will be scaling the magnets up to useful sizes, which may take years. In the meantime, it would be nice to know that these new magnets are competitive in their own right, and not merely because the cost of their competition is being driven up by regulation.

We Could Start By Repealing ObamaCare

Posted by Joshua Sharf in Business, National Politics, PPC, Regulation, Stimulus, Taxes on January 18th, 2011

President Obama claims in this morning’s Wall Street Journal to want to reduce the regulatory burden on American business, and so has ordered a review:

This order requires that federal agencies ensure that regulations protect our safety, health and environment while promoting economic growth. And it orders a government-wide review of the rules already on the books to remove outdated regulations that stifle job creation and make our economy less competitive. It’s a review that will help bring order to regulations that have become a patchwork of overlapping rules, the result of tinkering by administrations and legislators of both parties and the influence of special interests in Washington over decades.

I can remember hearing this sort of thing from every President since Jimmy Carter. You’ll note that the government is now considerably larger, more restrictive, and more intrusive than it was 35 years ago. Their failure is, in part, explainable by the nature of bureaucracy. Agencies fight interminable turf wars, and any attempt to systematically get them to play well together is doomed to failure. The FCC, for instance, insists on trying to regulate the Internet even in the face of specific Supreme Court decisions denying them the authority. Imagine how much more combative they are when the only opponents are other bureaucrats.

Philip Howard in his classic, The Death of Common Sense, notes how the USDA requires floors in certain food operations to be clean, while OSHA requires them to be dry. Good luck with that one.

The EPA has become a mini super-government unto itself, its authority reinforced by the automatic standing that many professional environmental lobbying groups have to bring suit on behalf of, “the environment.” Aside from trying to limit our breathing, ot currently is preventing the Border Patrol from patrolling parts of the border, meaning it’s exercising control not only over every aspect of manufacturing, it’s arrogating the right to regulate other federal agencies.

The FDA has tried, and will no doubt try again, to use price as a measure for approving medicine. As the president professes to be worried about medical innovation.

Of course, regulation isn’t even the major retardant of economic growth – government spending is. Obamacare amounts to a gigantic increase in the percentage of GDP explicitly devoted to government spending. The so-called stimulus hasn’t even been spent yet, largely because the same government didn’t know that there was no such thing as a “shovel-ready” project.

Coming after a miserable electoral repudiation of his policies, Obama’s comments recall President Clinton’s 1995 State of the Union Address. Realizing that he wouldn’t be able to push through large pieces of legislation, he famously declared that “the era of big government is over,” and embarked on a program of increasing regulation. Obama realizes much the same thing, but also recognizes that it will take years for bureaucracies, new and old, to absorb their new powers under Health Care reform, financial regulatory reform, and his expansive readings of executive authority.

Either Obama realizes this, and knows that he can give the appearance of understanding the problem without really giving substantive ground, or he doesn’t really understand the problem.

The subhead on his oped reads, “If the FDA deems saccharin safe enough for coffee, then the EPA should not treat it as hazardous waste.” Maybe we can get him to do the same thing with carbon dioxide.

If the FDA deems saccharin safe enough for coffee, then the EPA should not treat it as hazardous waste.

Slipshod Reporting on Rare Earths & Solar

Posted by Joshua Sharf in Backbone Business, Business, Energy, PPC, Regulation on January 16th, 2011

The Denver Post this morning reports that a lack of rare earths may be inhibiting the domestic solar cell industry. How this is so, they never quite describe. There’s no calculation, for instance, of what percent of a solar panel’s production cost comes from rare earths. Possibly, this is because rare earths aren’t actually used in the production of solar cells. According to a DOE study on strategic materials, solar cells use indium, tellurium, gallium, and maybe soon, selenium, none of which is in the lathanide series of rare earths. A briefing by the Rare Earth Industry Trade Association on the importance of rare earths to green energy applications doesn’t mention solar at all.

By coincidence, the New York Times this morning ran a piece on why solar panel manufacturers are relocating to China, and it seems that the reason has nothing to do with rare earths, which aren’t mentioned at all, and everything to do with our willingness to take the place of Germany and Spain in directing massive subsidies to the panels’ production. And in spite of our increasing mandates on so-called renewable energy as a source of electricity, it’s also not clear that we’ll be willing to force utilities to pay the exorbitant rates necessary to make large solar arrays profitable.

That, not the absence of a local rare earth supply, is what’s threatening a domestic solar industry.

I Volunteer Cheri Jahn

Posted by Joshua Sharf in Budget, Colorado Politics, PPC, Regulation on January 16th, 2011

Governor Hickenlooper has deservedly won praise for his idea of a “regulatory impact statement” for new regulations. Such a statement would estimate the costs to business of new regulations, and be a good step towards an actual cost-benefit analysis of new rules. Legislative Council already does something similar in the form of fiscal notes to new legislation. (Such a statement would only really be of use if the processes for determining the costs were as open as the results; it might be all to easy for a bureaucracy to game the system, or for large businesses to underestimate the costs to smaller competitors.)

So it was particularly interesting to see the following statement in this weekend’s Denver Business Journal from State Senator Cheri Jahn:

“When legislation comes through, the very first thing I am going to look at is: How will it effect my business and my ability to operate and to expand and to maintain what I am doing.”

“And if it is going to hurt me, I am not going to support it.”

Leaving aside the furor that would erupt if a Republican were to have said this – maybe only Jahn can go to China, so to speak – the sentiment is fine one.

Sen. Jahn serves on the Business, Labor, and Technology Committee, which has a 4-3 Democrat majority. If she really wants to have the information necessary to make the calculation she claims to want to make, perhaps she could sponsor the legislation required to make this happen. If she can’t be persuaded to do that, perhaps Sen. Shawn Mitchell could get her to vote for it. If it were to pass committee 4-3, it would certainly Senate Democrats in a bind on a floor vote.

As for the House, in the past, Democrats have balked at even estimating the cost of new health insurance mandates. This year, they wouldn’t have the votes.

Breaking New Ground

Posted by Joshua Sharf in PPC, Property Rights, Regulation on December 31st, 2010

When Kenneth Feinberg was appointed to politicize oversee the BP restitution process, many of us were worried that even under the best of circumstances, the government was forfeiting confidence in the process to gain some expediency. Now, it turns out that Feinberg was worried, too:

-

You are currently browsing the archives for the Regulation category.