Archive for category Colorado Politics

Moody’s Sees Bloomberg’s “Laughable” And Raises…

Posted by Joshua Sharf in Colorado Politics, PERA, PPC on July 13th, 2012

Being State Treasurer and trying to hold the Colorado Public Employees’ Retirement Association (PERA) to account can be a frustrating experience, as Walker Stapleton shared with Sean Hannity on Fox News Channel in June:

“I asked for some basic financial information about the defined benefit plan, where people were promised a rate of return, a massively inflated rate of return of 8%, Sean, that everybody from Warren Buffett to Michael Bloomberg have said is ridiculous and insane and preposterous. And they keep this rate of return promise, on purpose, to pervasively underfund the plan, and create a liability on the backs of our kids and their kids, and future generations of Americans.”

Now, it’s not just Mayor Bloomberg, it’s Moody’s.

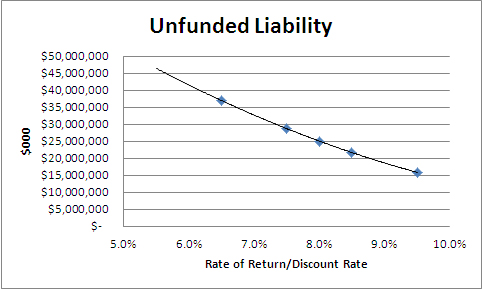

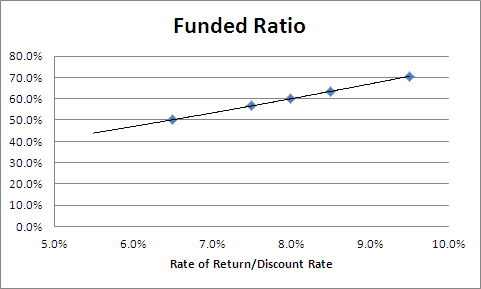

Moody’s Investors Service has asked for comment on a proposed adjustment to its valuation of the public pension liability in the United States. One of those changes would lower both the discount rate and the expected rate of return to a standard of 5.5%.

This would have the effect of tripling the estimated unfunded liability, from $766 billion to $2.2 trillion.

Trillion.

With a T.

PERA has more than 97,000 current benefit recipients receiving an average monthly benefit of nearly $3,000. It runs a sensitivity analysis on its liability, varying the rate of return and the discount rate from 9.5% (no adjectives need apply) to a merely overstated 6.5%. At 6.5%, it is barely 50% funded, and Colorado’s unfunded liability is just a shade under $37 billion.

A reasonable estimation back to 5.5% puts the unfunded liability at $45 billion, and the funded rate near death-spiral territory at 43.8%. I’m sure that when PERA releases its 2012 annual financial report in about a year, they’ll have done those calculations themselves. Here’s the recently released 2011 version.

Stapleton, a PERA board member, sued last year to get access to PERA records. That effort was rebuffed in Denver District Court in April.

“This is a battle for transparency that is going on all across our country,” Stapleton said on Hannity’s show. “It’s critical that we win this battle, because it’s critical for state budgets going forward.”

Amortize This!

Posted by Joshua Sharf in Education, Finance, PERA, PPC on July 6th, 2012

In Pension accounting, the amortization period is how long it would take to pay off the current unfunded liability, based on current contributions, and current employees.

Typically, pensions try to keep that time at about 30 years, or a normal, long career. That does a pretty good job of matching contributions to liabilities.

The amortization period for PERA’s school fund is now 59 years.

PERA’s retirement age is 58.

Retirees who haven’t even been born yet are having their benefits amortized by current contributions.

Sleep well.

Devouring the School Budget From Within

Posted by Joshua Sharf in Education, PERA, PPC on July 6th, 2012

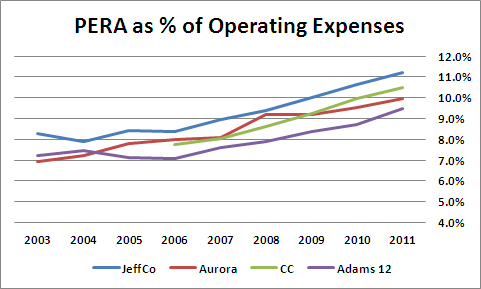

PERA’s problems don’t stop with the state. While the Colorado government has consistently shorted PERA on its Annual Contribution (theoretical) Requirement, local school districts have less flexibility in kicking the can down the road. As a result, their PERA contributions have increased rapidly, in some cases very rapidly, over the last decade or so. Here are the compound annual growth rates for four of the largest school districts from 2003 – 2011 (except for Cherry Creek, for which data was only available starting in 2006).

These numbers include all PERA contributions, both to the School Trust Fund and to the Health Care Trust Fund HCTF).

What does this mean for school budgets? Well, taking the Schedule 4 disclosures in the Statistical sections, we can derive the annual operating expenditures. For the government funds, we take the total expenses, subtract out the CapEx and the Debt Service, and then divide that number into the annual PERA contribution (described three years rolling in the Financial Section Notes).

The result? Not pretty:

The role of debt service in school finance is another matter well worth examining, but in this case, adding it in would just alter the level, not the trend. But consider that in JeffCo, 1 in every 9 dollars goes to PERA. In Cherry Creek and Aurora, it’s 1 in 10 dollars.

It’s not that school spending isn’t rising. It’s that PERA contributions are skyrocketing. And school budgets are starting to feel the pressure.

UPDATE: A typo in the Cherry Creek numbers prior to 2009 exaggerated the rate of increase, and created a “knee” in the data between 2008 and 2009. The 2006-2008 contributions were actually higher than I had reported. I’ve corrected the charts.

PERA – Wait Till Your GASB Gets Home

Posted by Joshua Sharf in PERA, PPC on June 29th, 2012

So we knew that when the new Government Accounting Standards Board requirements for public pension reporting came out, reported funding levels across the country would drop like a rock, but we didn’t really know how much.

Turns out that the good folks at the Center for Retirement Research at Boston College did some of that work for us a couple of years ago, studying 127 public pensions across the country.

Remember, the new standards have two parts: pensions must report their holdings at current market value, and not average those values over 3-5 years as they had before. And the unfunded liabilities, the portion that they do not believe are funded by current holdings, would have to be discounted at the long-term borrowing rate for the municipality involved, producing a blended rate likely lower than then expected return, and thereby decreasing the apparent funded level.

As of 2009, the numbers for Colorado didn’t look good at all. The school portion of PERA would fall from 65% funded to 52%, and the state portion from 63% to 48%. With current funded levels slightly lower, the actuals are also likely lower now.

It’s important to remember that these are accounting changes, and that the plans didn’t suddenly become less solvent overnight. But as a better reflection of reality, they are still pretty sobering.

Many Not-So-Happy Returns for PERA

Posted by Joshua Sharf in Budget, Colorado Politics, PERA, PPC on June 26th, 2012

As PERA prepares to release its 2011 Comprehensive Annual Financial Report, keep an eye on 2011’s returns. Treasurer Walker Stapleton understatedly calls 2001’s anemic 1.8% return, a “serious warning sign.” I’d call it a big, red, flashing LED billboard.

“What’s the big deal? It’s only one year,” I hear you cry.

Well, it turns out that if you’re projecting returns over a long period, the early returns have a disproportionate effect on whether or not you’ll make your targets. And while PERA projects an overly-optimistic 8% annual return, even meeting that as an average cumulative return is no guarantee of solvency to the end.

Returns aren’t smooth, they vary over time, and while the exact distribution is a matter of dispute, that fact isn’t. While the actuarial outlays are relatively smooth, returns can bounce around all over the place, and poor early returns can mean that you’re eating into your principal, and won’t be able to make it up on the back end, even if the returns rise to meet your project cumulative average.

Take three sets of return profiles, one constant, one with slightly higher-than-expected returns the first two years, and one where the fund loses 5% a year for the first two years, but settles in at a higher rate.

All of them converge to the save Cumulative average at the end of the 20-year run:

But because they have to take money out each year, the end of year balances tell a starkly different story for the three funds:

One fund slowly declines from $1 million balance to $800K. The one with higher early returns also declines, but ends up above its starting balance. And the one with poor early returns never recovers.

In fact, 20 data points is a very small sample, and even a distribution of returns that averages 8% could easily produce, over 20 samples, returns far higher or, more likely, far lower. The graph below shows the average returns and final balances from a 10,000-run Monte Carlo simulation:

Below about 10%, there’s a virtual guarantee that some of the funds will go bankrupt. Let me emphasize that this is a very simplified model, for display purposes only. Do not try this at home. (Actually, go ahead and try this at home. You’ll probably be as depressed and I was.)

What this shows, though, is that even using a lower rate of return doesn’t necessarily guarantee the fund’s soundness, and certainly doesn’t model the fund’s future. The only way to do that is through a Monte Carlo simulation, using the historical returns of the assets in which the fund is invested.

While more complex to do, and very hard to model on a spreadsheet, there is precedent for incorporating Monte Carlo modeling into financial planning, pension solvency analysis, and even into accounting. The Black-Scholes method, for instance, is used to calculate the value of stock options granted to employees and expensed on corporate financial statements. And allowances for bad debt are routinely audited for fidelity to previous customer defaults. There’s no reason that we couldn’t require pensions to do the same.

At the very least, it would perhaps keep today’s 1.8% return announcements from being such a surprise, and from taking such a toll on PERA’s solvency estimates.

Union Concessions Not So…Concessional

Posted by Joshua Sharf in Colorado Politics, Education, Labor, PPC on June 24th, 2012

This morning, the Douglas County Federation of Teachers responded to the School Board’s thoughts on the state of contract negotiations. The response is notable, because it appears to walk back a number of concessions that the union had made in earlier negotiations.

The union’s justification, laid out in a letter to its membership (see below), is that since the Board wasn’t negotiating in good faith, it has the right to rescind these concessions pending either mediation, arbitration, confrontation, or litigation.

Particularly, it appears to renege on two issues that it had agreed to defer to to the courts: the matter of union heads being full-time employees on the the district payroll (although all current expenses would be borne by the union), and union dues collection by the district.

Denver Democrats to Host Anti-Semitic Speaker at “Unity Dinner”

Posted by Joshua Sharf in Colorado Politics, Israel, Jewish, PPC on June 21st, 2012

Colorado Democrats, and even Denver Democrats, like to portray themselves as being more centrist, less likely to be run by their wing nuts. Certainly, there’s been little if any evidence of an anti-Israel bias in the state’s Congressional delegation over the years. Unfortunately, their choice of speaker for Saturday night’s State House District 7 “Unity Dinner” calls that claim into question.

The speaker is California Congressman Maxine Waters, who, only three months ago, was peddling Jewish conspiracy claptrap to the Women’s International League for Peace and Freedom, a hard-leftist organization:

AIPAC has a lot of power, a lot of influence. They raise a lot of money, and they raise this money not just for re-elections, but also to see that the people who will support their agenda are in key places in all of the committees. and all of the leadership of Congress. So they do exercise tremendous power, and I think that the more money you take from AIPAC, the more you get tied down to their policies. I do not accept contributions from AIPAC.

Well, that’s mighty independent of her, given that AIPAC doesn’t make campaign contributions, spending its money on lobbying. Make no mistake, there are plenty of pro-Israel PACs, an they are often informed by AIPAC as to the positions of Congressmen on specific bills or appropriations. But AIPAC doesn’t even issue legislative ratings. So if Rep. Waters wants to stay clear of undue Jewish influence, it’ll take more than dodging non-offered contributions from a non-existent PAC. (The PAC in AIPAC stands for “Public Affairs Committee.”)

What’s disturbing is that the Denver Democrats would choose someone like this to speak at a Unity Dinner. The last couple of years, they’ve had more or less traditional liberals speak at their Jefferson-Jackson Day dinner: Cory Booker, Deval Patrick.

And, typically, the choice has evoked no response from the establishment Jewish institutions here in Colorado, dominated as they are by those who identify Jewishness with membership in the Democrat party.

Democrats on Vote Fraud: What, Us Worry?

Posted by Joshua Sharf in Colorado Politics on June 20th, 2012

Obama Wins, 9% – 42%

Posted by Joshua Sharf in Economics, Media Bias, PPC, President 2012 on June 7th, 2012

The last jobs report was about as bad as it could have been without actually putting us back in recession. A downward revision of April’s job creation, coupled with a May net of 69,000 wasn’t even enough to keep the unemployment rate flat. The last 27 months of anemic growth have let the rate drift down only because massive numbers of Americans are giving up looking.

Almost everyone who was paying attention knows this was a bad report. A Gallup poll had 9% of people calling it positive – probably people who think anything not negative is good, or people who found jobs – while 42% called it negative to some degree. Ten percent had no opinion, and 40% called it “mixed,” which is pretty much the “no opinion” for people who don’t want to admit they weren’t paying attention.

Naturally, Postblogger Ezra Klein runs a piece headlined: “Most Americans didn’t think the last jobs report was bad news.” It’s true that the number of people who think things are getting worse hasn’t gotten worse, and the additional 3% who think rate it “poor” is pretty much statistical noise.

But people can go a long time before realizing that changes are permanent. In the mid-90s, I worked for a while in Johnston, Pennsylvania, and many people talked about how they were waiting “for the Mill to come back.” The Mill had been closed for many years, and wasn’t coming back, that, or any other century.

The economy can tread water for a long time, not getting better or worse, slogging along an a Euro-stupor, or a sushi-style lost decade. People won’t necessarily rate things as getting worse, even though they know they’re not getting any better.

But that doesn’t make losing 9-42 any less of a loss.

PERA, the Unions, and You

Posted by Joshua Sharf in Education, PERA, PPC on June 3rd, 2012

One of the less-noticed points of contention at Douglas County’s open negotiations the other week was the status of school district employees who are actually on the union payroll. Basically, union heads leave the classroom to spend their time representing teachers and the union, yet remain officially school district employees. The district wants to end this practice, and in fact, pick-slipped the union heads a couple of weeks ago. The union wants to retain them as district employees, and claims that this is a non-issue, as the union reimburses the district for the employees’ salaries and PERA contributions.

The problem isn’t the current costs – although there may be some conflicts of interest in having a union boss refuse supervision and evaluation by the district, while still remaining nominally an employee. The problem is PERA, and its something that the retirement plan ought to look at.

What happens here is that the unions, the national, state, and local, pay this employee’s salary. That salary is no longer determined by the seniority or performance measures that apply to all other teachers, but by the people actually paying the salary. So that employee is no longer being paid on their value to the district, or to the students, but to the union. Their PERA benefits, which, over their lifetime, are calculated based on that salary. Which means that PERA is paying benefits to potentially hundreds of employees statewide based not on their service to the taxpayers, but on their service to the union. And since those benefits will, as currently constituted, far exceed the amount paid into the system, they constitute a net payout to the union, which doesn’t have to cover their own employees’ retirement benefits for those year.

The union will say that it’s unfair that a teacher should have to give up earned retirement benefits when they become a union rep. But of course, they don’t have to give up anything they’re vested in. This is, in the end, no different from a bureaucrat or a regulator leaving to take a job as a lobbyist. They’re no longer directly serving the state government, and should no longer be a part of the state government retirement system, except for the benefits they have earned. The union will argue that this will make becoming a union rep a much less desirable position, but never explain why that desirability should come at the direct expense of the taxpayer rather than the union and the teachers it represents.

-

You are currently browsing the archives for the Colorado Politics category.