In yesterday’s Denver Post, PERA’s Chief Investment Officer, Jennifer Paquetteis, responded to an op-ed by investment professional Blaine Rollins (“Hope Is Not An Investment Strategy“) that detailed the risk that PERA has taken on:

PERA has instead relied on solid investment strategies created under the direction of the board of trustees with the help of highly experienced staff and consultants. PERA’s investment strategies match its mission, with an investment horizon of decades and a focus on maintaining the stability of the fund.

…

These investment returns allow PERA to provide reasonable benefits for public servants without placing an excessive burden on taxpayers.

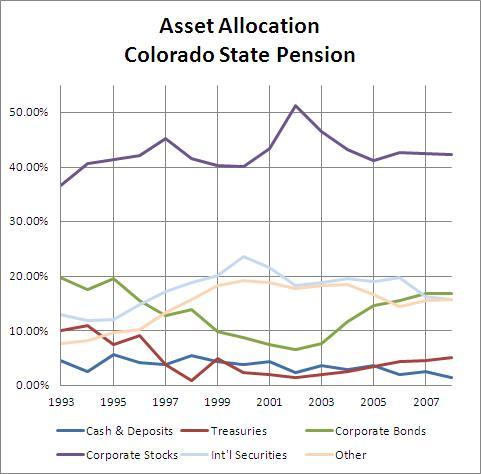

In a previous post, I noted that as a whole, US government pensions had shifted to taking on more risk over time. Interestingly, this does not appear to be the case with PERA:

Seeing that stocks, as they appreciated in 2002, were becoming a disproportionately large share of the portfolio, managers shifted those investments to corporate bonds, which tend to have lower yields, but generally assume less risk. They have also – albeit slowly – grown the proportion of their investment in Treasuries. While I believe that PERA’s overall investment mix still has entirely too much risk built in, it is hard to argue that they have gone around chasing higher yields, or allowed their asset allocation to get out of whack when one class outperformed the others.

The problem is, Ms. Paquetteis’s conclusions don’t necessarily follow from her premises, especially over the long term. Paquetteis’s response only addresses whether or not PERA is following reasonable portfolio diversification techniques. It fails to address the underlying problems with those techniques: the large unfunded liability, the added year-to-year risk associated with needing larger and larger returns, and the faulty accounting standards that not only permit, but actively encourage taking on that extra risk.