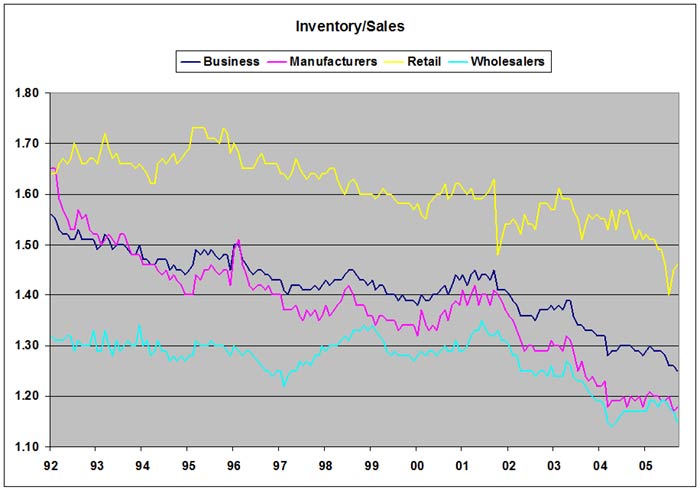

One of the great success stories of American business over the last 20 years is inventory management. Take a look at the inventory-to-sales ratio over the last 20 years:

Overall, businesses have to carry less than 3/4 as much inventory as they did 14 years ago to fulfill the same number of orders. For manufacturers, that number is 5/8. Multiply that by the overall growth in the GDP, and the savings are staggering. In fact, manufacturing efficiency is really driving this improvement. The correlation between the overall number and manufacturing is an astonishing 0.98. So while resellers are getting better at inventory mangement, most of the improvement comes from innovations like Just In Time manufacturing.

This is both a cause and a result of technology, as better processes free up money for capital investment, which further increases efficiency. To the extent that American manufacturers haven't been run off the playing field altogether, this is why. To be fair, other factors such as proximity to markets help. More clothes are being produced in smaller quantities locally, as a futher aid to flexibility. And some of the biggest adopters of just-in-time are the welfare states known as the auto companies, so all they've done is stave off the inevitable. But auto producers aren't nearly as big a part of the economy as they used to be, so these efficiency gains are quite real.

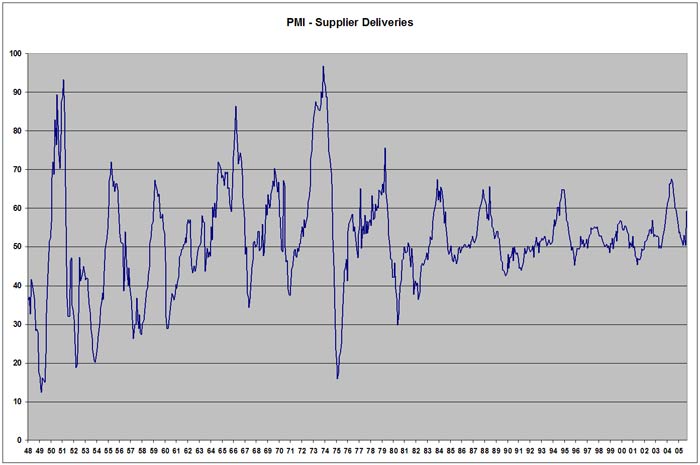

This doesn't come without a price, however. In this case, it's a loss of flexibility. If that truck with the spare parts isn't there on time, you're less likely to have a box of them lying around on the shop floor. Take a look at the PMI survey component called Supplier Deliveries. Over 50 means that supplier deliveries are getting slower:

Whoa. Better processes mean more stability - a lot more stability -, but since 1992, only rarely have purchasing managers seen actual improvemet in the month-to-month situation, and that improvement tends to be correlated with economic slowdowns. (No, 1996 wasn't an actual recession, but there was a good deal of grumbling that Greenspan had tapped the brakes hard enough for most of us passengers to spill our coffee.) Now maybe some of this is just purchasing managers always worrying about where their next bucket of bolts is coming from, but there must be more to it than that, otherwise why ask the question?

None of this should be too surprising. Robert Bruner, in his M&A How-Not-To book, Deals From Hell, notes that tight coupling, or loss of flexibility, lets trouble propagate through a business much more easily. And what's true for individual companies is true in the aggregate.

Now, it would be interesting to see how many of these slow deliveries are raw materials, and how many are manufactured goods. Given China's recent propensity for trying to lock up raw materials and resources, a lot could be riding on that answer.