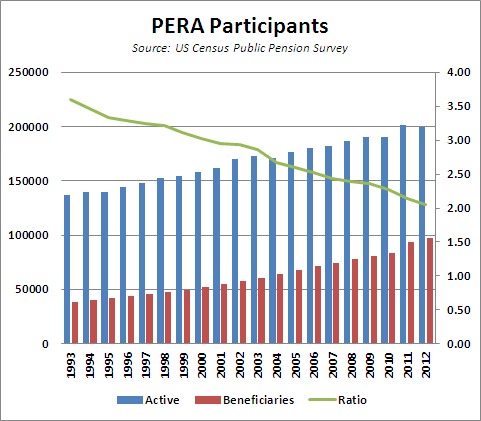

This chart is more or less self-explanatory. Over the last 20 years, the number of workers per beneficiary within PERA has dropped from about 3.6 to just over 2.0:

PERA’s CAFR includes the following disclaimer:

By itself, a declining ratio of actives to retirees and beneficiaries does not pose a problem to a Division Trust Fund’s actuarial condition. However, to the extent that a plan is underfunded, a low or declining ratio of actives to retirees and beneficiaries, coupled with increasing life expectancy, can complicate the Division Trust Fund’s ability to move toward full funding, as fewer active, contributing workers, relatively, are available to amortize the unfunded liability.

This is about right, although even a fully-funded system won’t stay fully-funded for very long under these conditions. Indeed, PERA was fully-funded as late as 2001. In the 90s, PERA’s long-term problems were masked by a tech bubble, and when that burst in 2000, the fund started to fall into an under-funded state that it’s never recovered from. Since under an underfunded defined-benefit plan, current expenses have to be paid for out of current contributions, and fewer workers are pulling the cart for each retiree, the deficient horsepower will have to be supplied by the taxpayers.